The Global Economic Outlook in 2023

27th January 2023

What should we expect from the global economy in 2023? To answer this question we welcomed Jens Eisenschmidt, Chief European Economist at the investment bank Morgan Stanley, to give an online presentation to a large audience of Eden McCallum clients and colleagues. Jens Eisenschmidt is based in Frankfurt and heads the European Economics team, and his presentation also drew on the research and analysis of Morgan Stanley colleagues in the US and Asia.

Eisenschmidt began by observing that in general prospects for 2023 look a bit better now than they had done in the autumn of 2022, a view echoed in our recent Economic and Business Outlook Survey. Even though a slowdown is underway, inflation has probably peaked and consequently we may be approaching the last round of interest rate rises. This gives some cause for optimism.

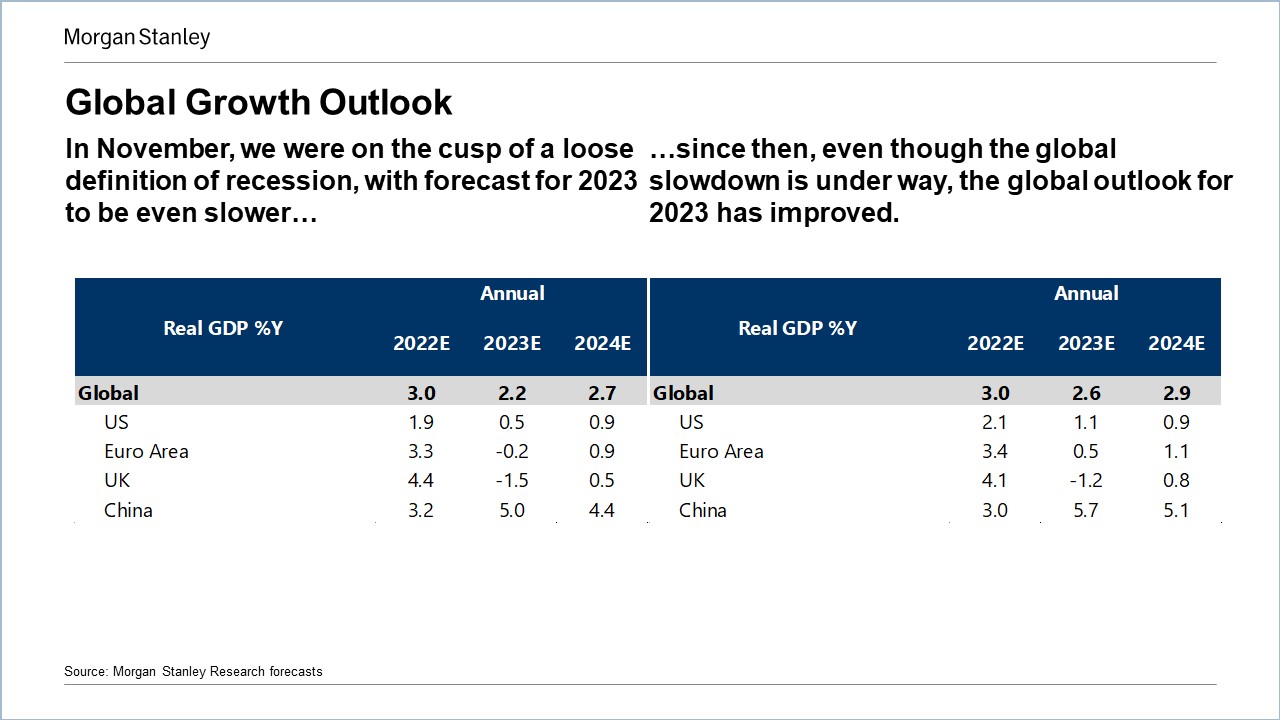

All the same, Morgan Stanley’s current global GDP growth forecast of 2.6% for 2023 is still rather bearish, Eisenschmidt said. (Anything under 3% is.)

The headline forecasts for the world’s major trading zones are that the US is heading for a deceleration but not a recession. The euro area is in a significant slowdown but looks set to avoid a technical recession. The UK cannot avoid recession. And China, coming out of lockdown, will see growth of 5.7% in 2023.

Along with easing inflation, the fact that natural gas prices have fallen, in the context of a mild winter, has helped growth expectations. The speed of China’s return to more normal working conditions has also been a positive surprise.

There are still obstacles to higher growth rates, however. Inflation remains high in the UK and the rest of Europe, which is having an impact on consumption. Monetary tightening in the US has been rapid and aggressive.

In geo-political terms, the world is becoming less collaborative, Eisenschmidt noted. There is now long term strategic competition between the US and China, with tensions over the manufacture and supply of semiconductors, for example. The US Inflation Reduction Act (IRA) presents a challenge to the UK and Eurozone areas, as it could make the US a natural home for renewable energy businesses, and the IRA marks a ‘seismic’ shift in global trade, with its inherently protective measures.

China

Morgan Stanley forecasts quite strong growth in China this year of 5.7%, driven by a strong rebound in demand for services. But inflation is not expected to be a problem, as the labour market has been weak and pay is not about to rise dramatically.

US

The Fed’s tightening of monetary conditions has been carried out rapidly. Morgan Stanley was surprised through 2022 how well the US economy held up. While inflation is set to fall, the risks of recession have risen. The rate rise of 1st Feb may turn out to be the last of the current cycle.

UK

Eisenschmidt characterised the UK as a “problem child” of the world economy. Morgan Stanley forecasts a year-on-year 2% peak-to-trough fall in GDP. Persistent high inflation will take a toll on disposable incomes and will hit consumer spending. In economic terms, Brexit is putting friction and cost into the economy. And a continuing tight labour market may limit the UK’s growth potential. Like the Fed, the Bank of England may be reaching the end of its current rate rises. Rates could come down in 2024 to 2.5%.

Euro area

The contraction of the Eurozone economy will be less pronounced than in the UK, Eisenschmidt said, but growth will be well below potential, at perhaps 0.5% in 2023 and 1.1% in 2024. Labour markets remain tight. The public sector has absorbed a lot of people and the services sector may struggle to recruit the staff it needs. Wages will lag behind inflation, leading to a fall in real incomes.

Inflation should fall to 5.4% in 2023 and 2.3% in 2024. Improvements in the natural gas market (both lower than expected prices and better storage) are positive for growth prospects. Interest rates may peak at 3.25% this spring.

Closing comments – IRA

Eisenschmidt’s closing comments in the main part of his presentation touched again on the US Inflation Reduction Act (IRA). This legislation, he said, was a loud signal from Washington that it wants businesses to invest in America. This represents a challenge to other nations and markets, and global trade in general. The EU is moving fast to respond. How will other countries react, and will this lead into a downward spiral of protectionism?

Q&A

In a brief question and answer session, Eisenschmidt was asked to say more about the IRA and its consequences. The EU has been stirred into action to try to moderate the US proposals, without much success. It could have a significant impact on the prospects for investment in Europe.

On the 9th and 10th of February there will be a meeting of the European Council where the EU’s response will be discussed further, possibly involving a relaxation of state aid rules to enable more investment.

Net Zero is a “gigantic opportunity”, Eisenschmidt suggested, but a proper European response will require co-ordinated political action.

Demographics are another challenge. Labour markets in Europe remain tight and there is a need for migration. Germany alone requires between 400,000 and 500,000 new arrivals every year.

While Eisenschmidt sees signs of recovery in the global economy, the headwinds are challenging. US/China relations are increasingly difficult, and internationally there is less rather than more integration (sometimes described as “deglobalisation”).

This reality check should temper over-exuberance in stock markets and elsewhere. We are not out of the woods yet.

To view the full presentation (video), please click here

To see the slides presented, please click here

Follow us on LinkedIn to remain updated.