Lord Turner – Net Zero: Prospects for a Green Economic Recovery

One year ago, Lord Turner spoke at Eden McCallum’s inaugural event on the prospects for a world of “net zero” carbon emissions. Twelve months on, but this time via Zoom, he gave a detailed update on progress and the state of the energy debate internationally. He is ideally placed to do so as the Chairman of the Energy Transitions Commission, a global coalition of major power and industrial companies, investors, environmental NGOs and experts working on pathways to achieving net-zero emissions by mid-century. Here we share Lord Turner’s perspective on what has changed over the past year and the future outlook.

How likely do you think it is that we can meet net zero targets?

The goal, supported by the Intergovernmental Panel on Climate Change (IPCC), is for the world to achieve net zero emissions by the middle of the century, including very significant reductions in the coming decade of between 40% – 50%.

The good news is that the Energy Transmissions Commission is certain it is technologically and economically possible to get to net zero emissions by 2050. All developed countries should get to net zero by 2050, and all developing countries should get there by 2060, at the latest, and earlier if possible.

The science is pushing us all the time to be more ambitious.

What are the factors which make you believe this goal is attainable?

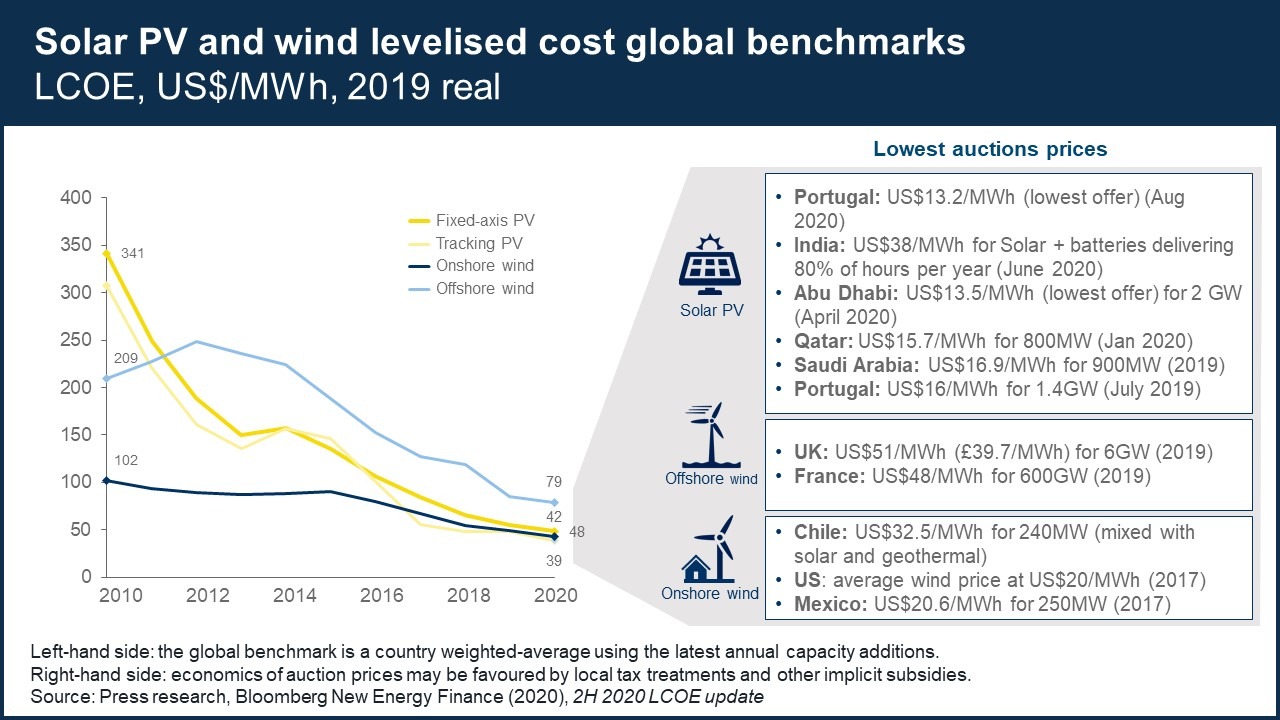

Developments in solar PV and wind, batteries, and hydrogen make a zero carbon economy possible and have accelerated in the past year. There has been a revolution in the cost of renewables in the last ten years.

For example, the cost of solar energy is now 10% of what it was in 2010. An auction to generate solar photovoltaic (PV) energy in Portugal in August last year was fixed at $13.2 per megawatt hour (MWh), that is 1.3c per KWh, or 1p per KWh. In the UK, customers pay around 15p per KWh for electricity (including the costs of transmission). The generation costs of solar power are now becoming a trivial amount and solar PV costs are going to keep coming down.

The cost of wind energy has come down between 60% – 70%. There have been dramatic falls in the cost of offshore wind energy in the last five years.

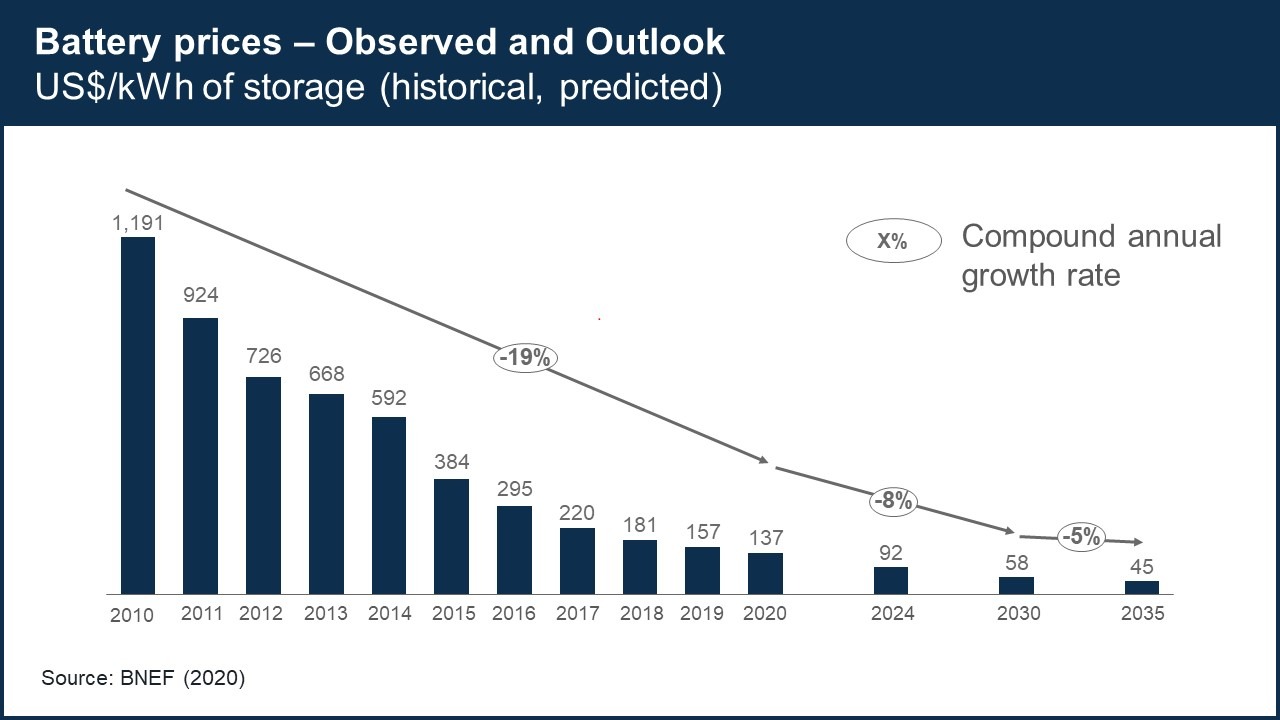

The storage of electricity is also getting cheaper as the cost of batteries has collapsed. Between 2010 and 2020 the cost per kilowatt hour storable of a lithium ion battery fell by 19% per year, from well over $1,000 to just over $137, a fall of almost 90% in total. There has been no slowdown in this fall in recent times. The expectation is that the cost of storage will fall to under $50 per KWh by 2035. At $100 per KWh an electric vehicle (EV) passenger car becomes cheaper to buy upfront than an internal combustion engine (ICE) car. This is in addition to the lower costs of ownership and running an EV.

A third important technological development is that the cost of electrolysis, to make hydrogen, is set to fall. A prediction is that the current cost of electrolysers of $850 per KW of capacity will come down to $200 by 2030 and $100 by 2050. Once you start developing something at large scale the opportunities for cost collapse are huge – green zero carbon hydrogen is within reach.

What are the implications of these technical and economic developments on progress towards the overall net zero goal?

The three technological trends outlined above have accelerated in the past year. They mean that, firstly, we can decarbonise electricity production at zero cost to the consumer – solar and wind are now cheaper than coal and gas, certainly on a new build basis. Secondly, batteries solve the day-to-night challenge of providing renewable electricity when the sun doesn’t shine and the wind doesn’t blow. The challenge in providing heat in winter in north west Europe is different – hydrogen may have a role to play. Taken together, 85% of variable electricity supply can be generated with renewables at a competitive cost.

What are the implications going to be for the energy sector?

A zero carbon economy requires massively more electricity. Demand for electricity globally could rise almost four-fold by the middle of the century and there could be a ten-fold increase in the use of hydrogen by the same date. Today about 20% of the energy we use is in the form of electricity, by 2060 it will grow to over 60%. At the Energy Transmissions Commission, we forecast the use of thermal coal falling by 95%, oil by 80% and gas by 50% by 2050.

What are the implications for sectors with high energy usage?

Surface transport will be completely electrified, either in a battery electric form or in a hydrogen fuel cell form. The sale of new internal combustion engine cars will be banned in the UK from 2030. Car companies – GM, Ford, JLR – are committing to help meet this target and Skandia trucks and Volvo are also heading in this direction.

Then there are the “hard to abate” sectors: aviation and shipping, cement, steel and petrochemicals. These are much harder to electrify, but technologically feasible routes are emerging to decarbonise these sectors. Carbon capture and storage (CCS) can help with cement, for example. You see companies in these sectors making net zero commitments: Maersk has committed to becoming a zero carbon shipping company by 2050; Arcelor Mittal and Baowu steel in Shanghai (the world’s largest steel maker) have both made net zero commitments, to be achieved by 2050; Shell and BP are aiming for net zero in their operations and also in how their customers use their products.

How much geopolitical will is there to achieve net zero targets?

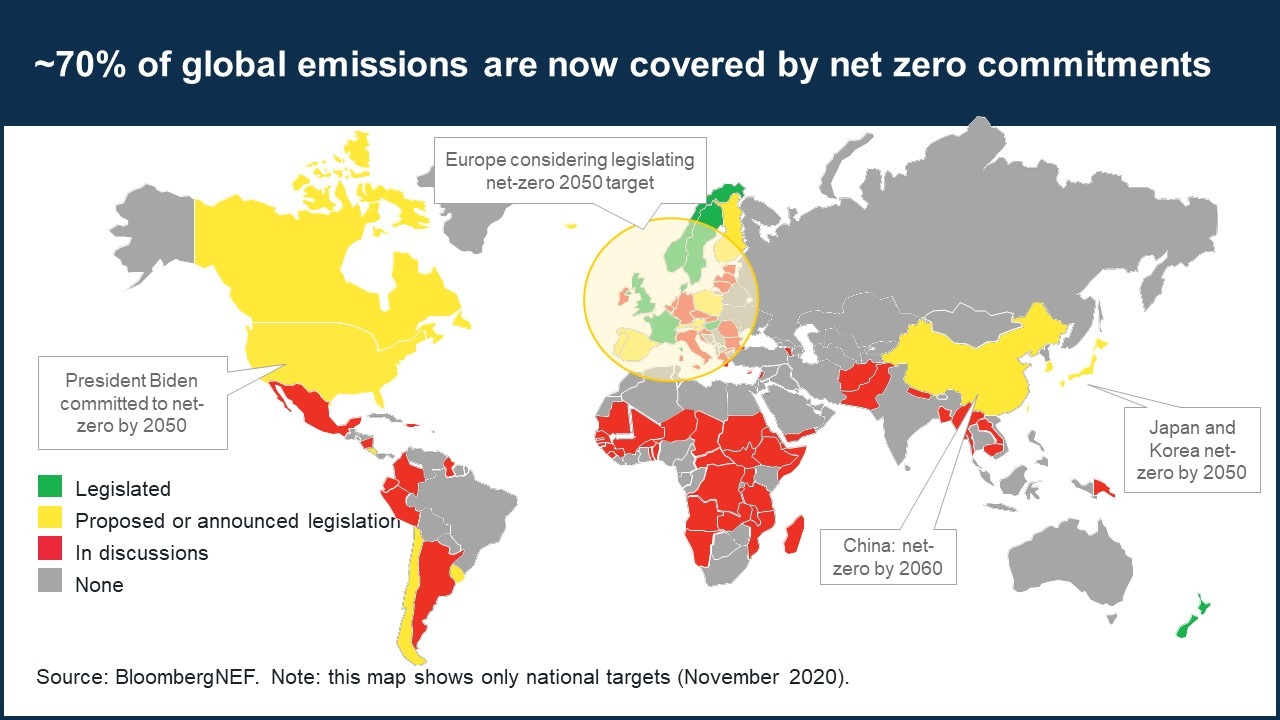

More and more countries are making commitments to achieve net zero carbon targets and the last year has seen several moves. In September at the UN, President Xi committed China to achieving zero carbon emissions by 2060. Korea and Japan followed and committed to hitting a 2050 target. The election of President Biden changed US policy: they have now committed to reaching net zero by 2050. The COP 26 summit in Glasgow in November is providing further impetus to these developments and there should be more announcements over the course of the year.

70% of global emissions are now covered by net zero commitments from governments around the world, and that was not the case a year ago. Commitments made by political leaders create a ratchet effect. Business has some certainty about the policy framework and alters course accordingly.

What is the economic cost of reaching net zero?

The costs keep coming down. Lord Stern’s report in 2005/6 said that to get to net zero by 2080 would cost 1.5% of global GDP, with 60% reductions possible by 2050. When I first chaired the UK’s Climate Change Committee (CCC) in 2008, it was thought an 80% reduction by 2050 would cost 1.5% of GDP. When the CCC reported in December last year it said that getting to net zero in the UK would cost just 0.5% of GDP – the costs keep falling.

In the UK, costs will continue to fall in transport and generation. The big challenge is residential heating, where the cost of improved insulation for some of Britain’s poor quality housing is high, and decarbonising residential heating (replacing gas boilers with heat pumps) will be expensive. But overall, balanced out, the costs to the consumer of zero carbon electricity will not be great. For business, investment will lead to operating net cost savings by 2050.

Across the world there will need to be an additional investment of 1% – 1.5% of GDP from now to 2050 to build an electricity system which will give us green electricity on a close to zero marginal cost.

For the consumer, the increased costs borne by shipping or steel companies to decarbonise will not be felt as a big percentage in the purchase price of finished goods. At wholesale business to business level, the costs are more significant. Everyone has to decarbonise at the same time, otherwise costs will not be shared on a fair basis by all.

Do we need to reduce consumption or will technology enable us to continue living as we do and for the developing world to increase its living standards, while still achieving net zero?

I refer to this as the Greta vs Elon debate – and of course it is not a simple binary choice. Many sensible people rightly support a balanced mix of both approaches and philosophies.

Across many economic activities and forms of consumption, there are in the long term almost no relevant planetary boundaries – with no limit to how much green electricity we can sustainably produce and consume, and therefore no long term limits to how much we can heat or cool our homes , drive our electric cars or fly. This is the arena of physics and inorganic chemistry, and the use of photons, electrons and ions.

But conversely, there are severe and immediate planetary boundaries in other sectors of the economy, and in particular in relation to food and textile production, which may require dramatic behavioural change, and in particular diet change, if we are to avoid ecosystem disaster. Meat-related emissions are significant and so either reducing meat consumption or the greater consumption of meat substitutes may be necessary. This is the arena of organic chemistry and biology, of everything to do with life on earth, of photosynthesis and the production of complex hydrocarbon, carbohydrate and protein molecules, where we must recognise inherent planetary boundaries which we are already going far beyond.

To listen to the full event recording, click here and follow us to remain updated on further sustainability initiatives.