Eden McCallum Consumer Sentiment Survey Q3 2025

Consumers in the UK and the Netherlands are looking watchfully to the future, making carefully considered spending choices as they wait to see how the political and economic situation develops. This is one of the main messages to emerge from the latest Eden McCallum survey of consumer sentiment, carried out this summer.

Around two thousand people in each of the two countries were asked to reflect on their overall sentiment and spending decisions and the reasons behind them.

The backdrop to the respondents’ spending decisions is an uncertain world in which inflationary pressures are still a concern. Little wonder, then, that shoppers are weighing up their choices carefully.

Economic and political context

In both countries more people express optimism than pessimism about the future, but the positivity is not overwhelming. Under half of respondents – 45% – are optimistic about the future. Pessimism is higher in the UK, where 34% are gloomy and 21% neutral. In the Netherlands only 21% of people describe themselves as pessimistic with 34% neither optimistic nor pessimistic. In neither country has pessimism returned to 2022 levels, which marked the recent low point in outlook.

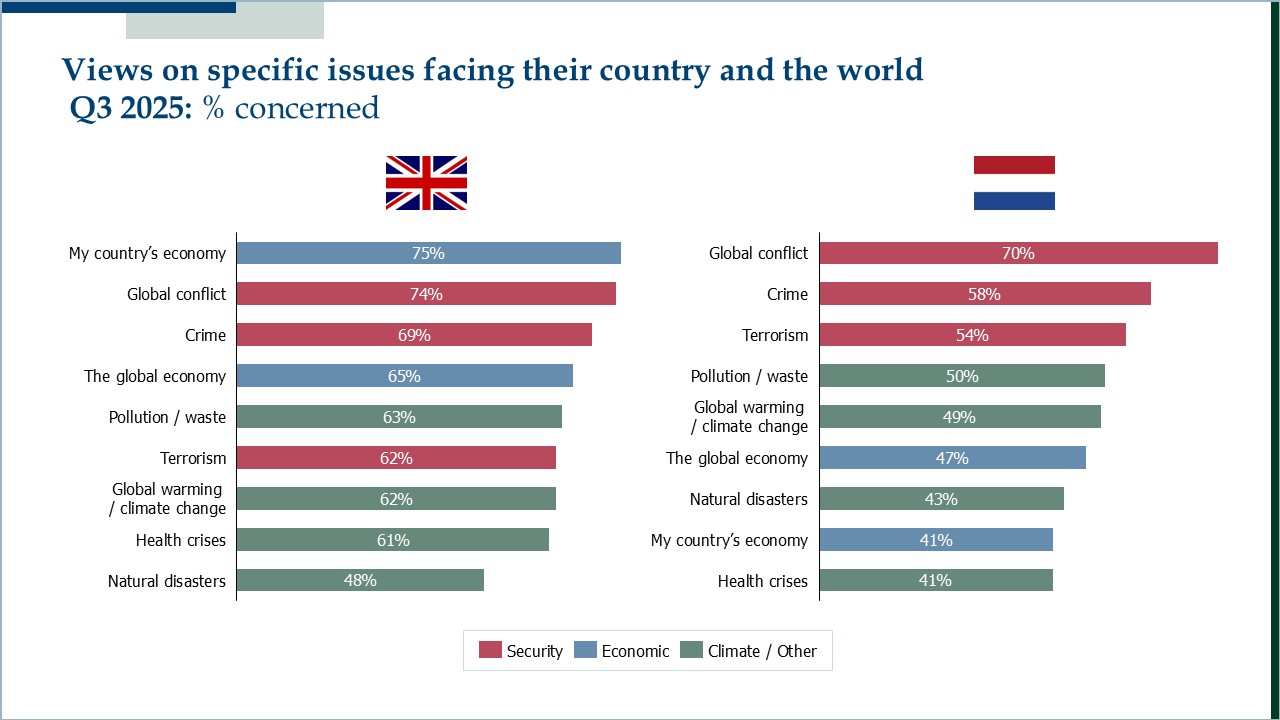

British worries centre mainly on the domestic economy (75% are concerned) while in the Netherlands the issue of global conflict is the principal cause of anxiety (70% cite this).

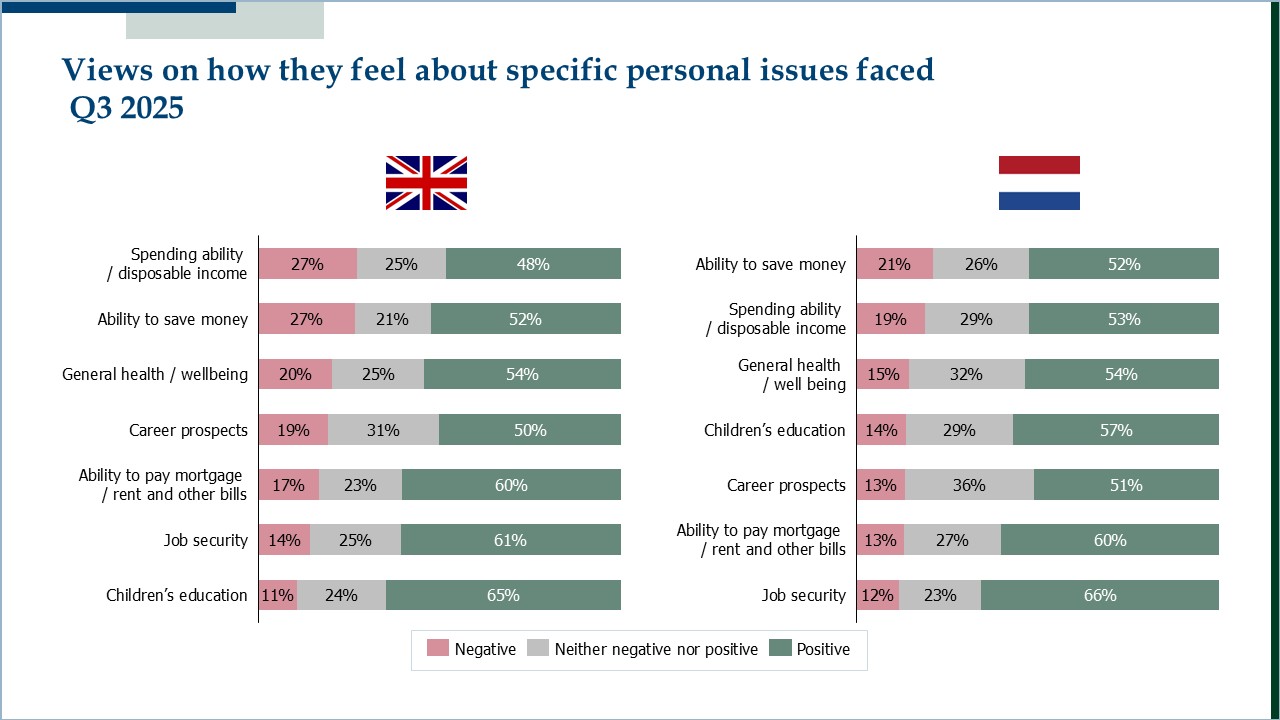

27% of Brits and 21% of Dutch consumers feel negatively about their ability to save money, and similar percentages are concerned about their disposable incomes. However, this is outweighed by the 52% of respondents in both countries who are positive about their ability to save money. And in general, on personal issues, positive views comfortably outweigh negative ones in both countries across a range of topics – health, career, ability to pay the mortgage, and so on.

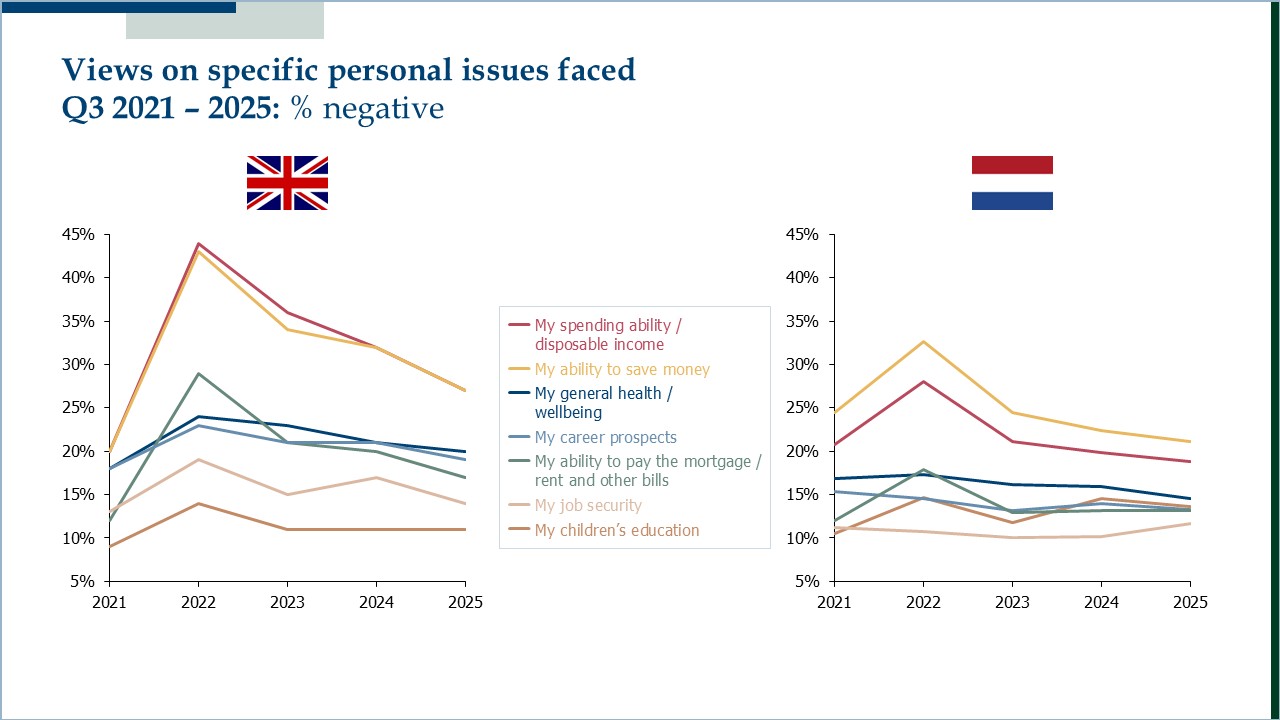

Since its peak in 2022, when the war in the Ukraine began and energy prices led to a spike in inflation and interest rates, negative sentiment on personal issues has been reducing in both countries. In the UK, negativity is down on almost every factor we measured.

Spending

We have grouped consumer spending into three separate categories: “essentials” (which comprises groceries, broadband and mobile), “fashion and home” (which includes homeware, beauty and personal care products, and children’s clothing and toys), and “entertainment” (which includes restaurants, takeaways, out-of-home and digital entertainment, alcohol and tobacco).

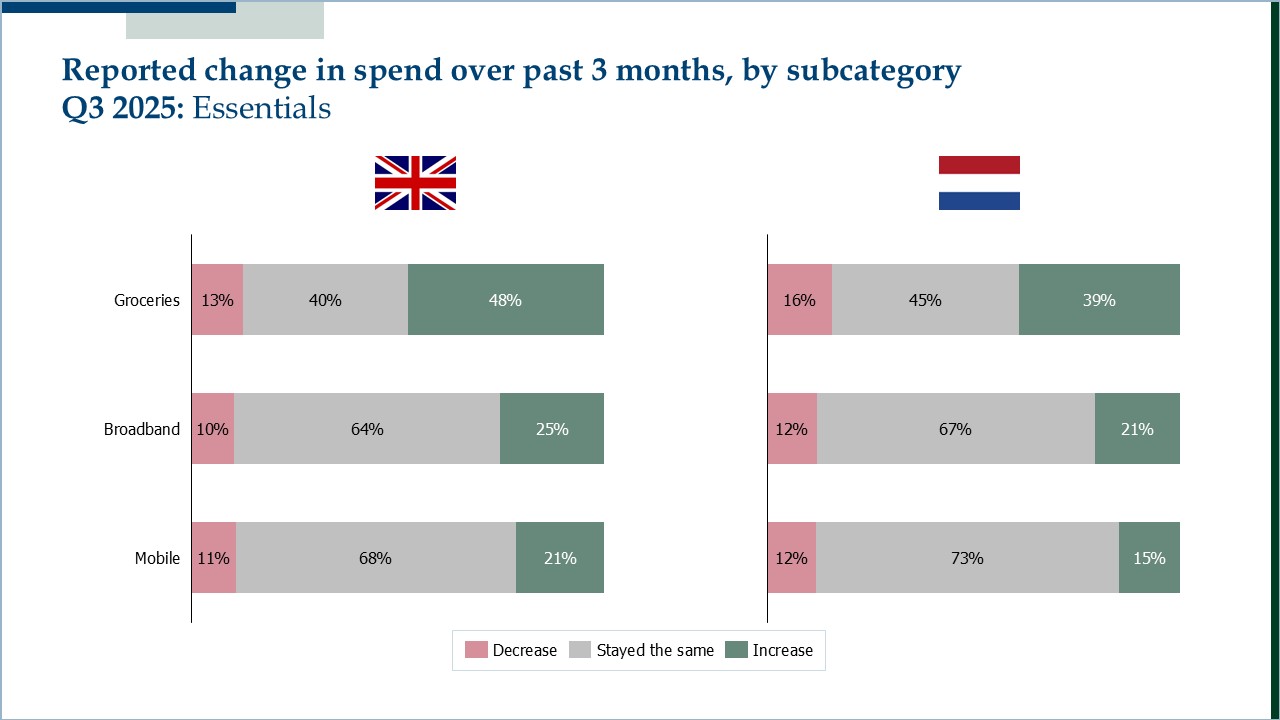

Spending – essentials

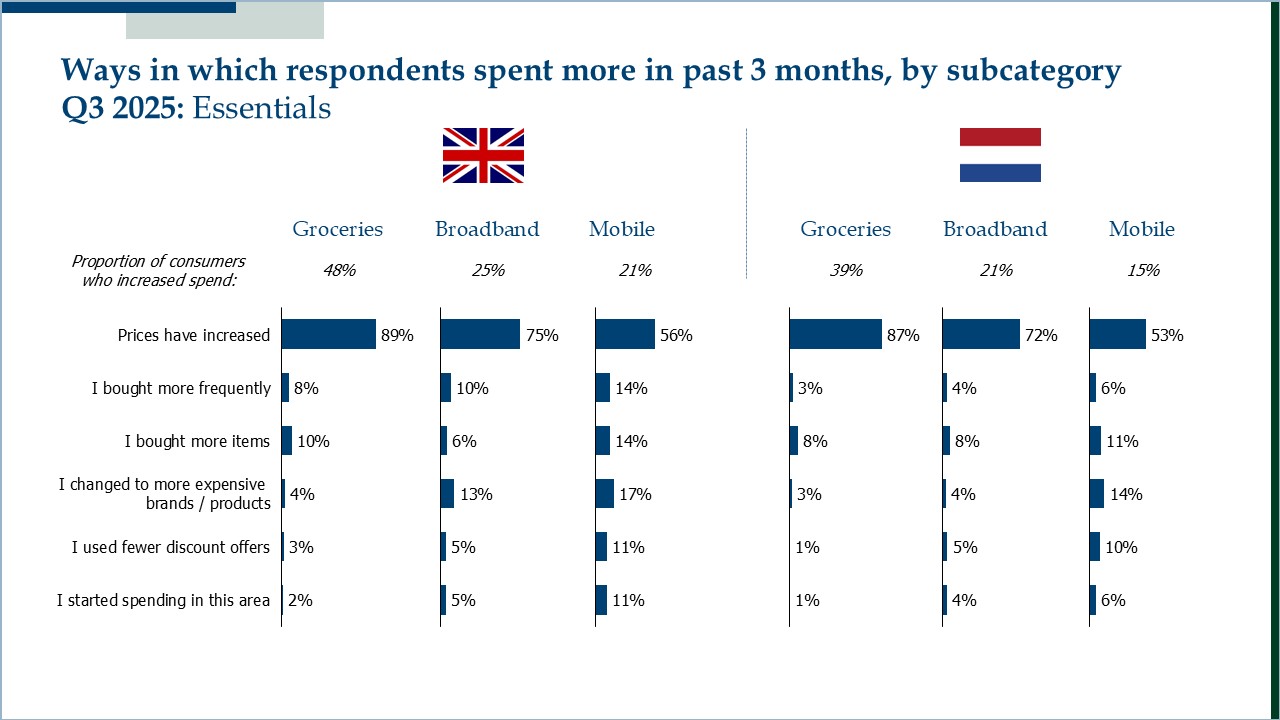

In both countries spending on groceries has increased. 39% of Dutch consumers are spending more and only 16% are spending less. The gap was even larger in the UK: 48% are spending more and only 13% less. In both cases, higher prices lay behind this increase in spending. More is also being spent on other essential items, broadband and mobile, for the same reason. In other words, inflationary pressures on essential items cannot be avoided and are very much “front of mind” for consumers, causing a diversion of spend to these categories.

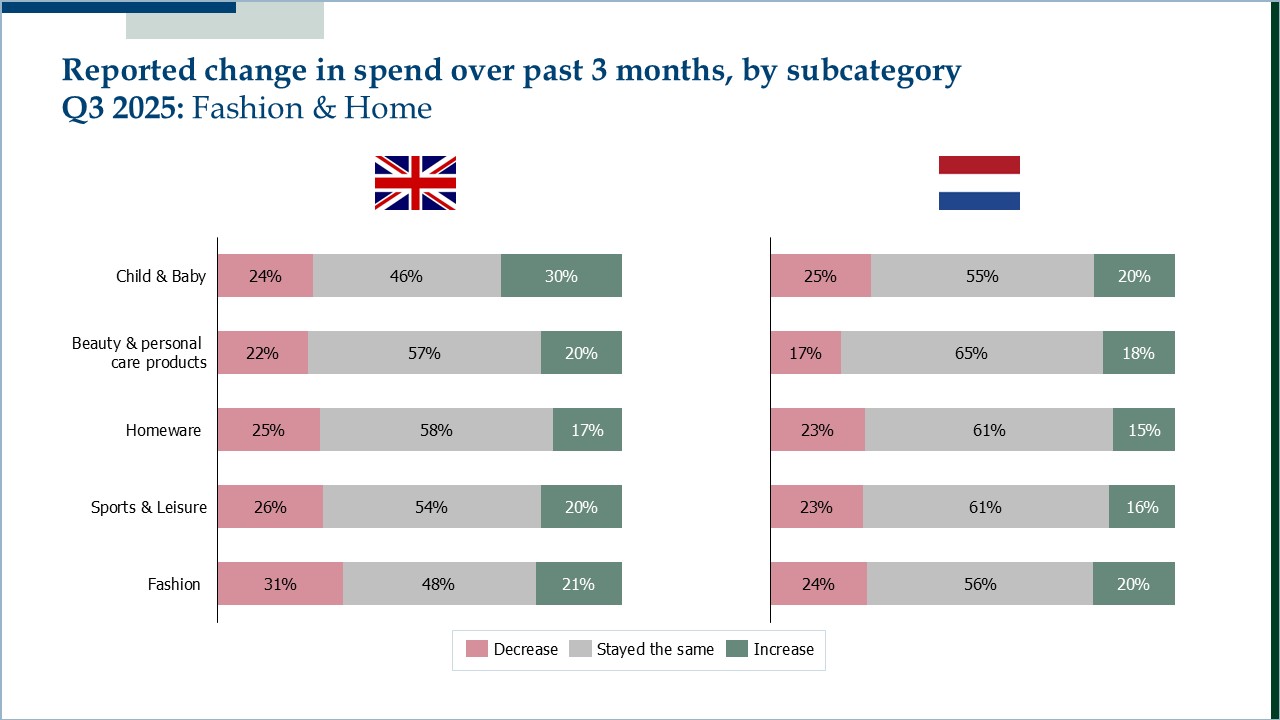

Spending – fashion and home

On discretionary items more consumers are, by and large, reducing spending in most product categories than are increasing it. For example, 23% of Dutch consumers have reduced spending on homeware while 15% have spent more. In the UK, 31% are spending less on fashion items while 21% are spending more. Simply choosing to buy fewer items is the main reason for this reduced level of spending (see below).

Spending – entertainment

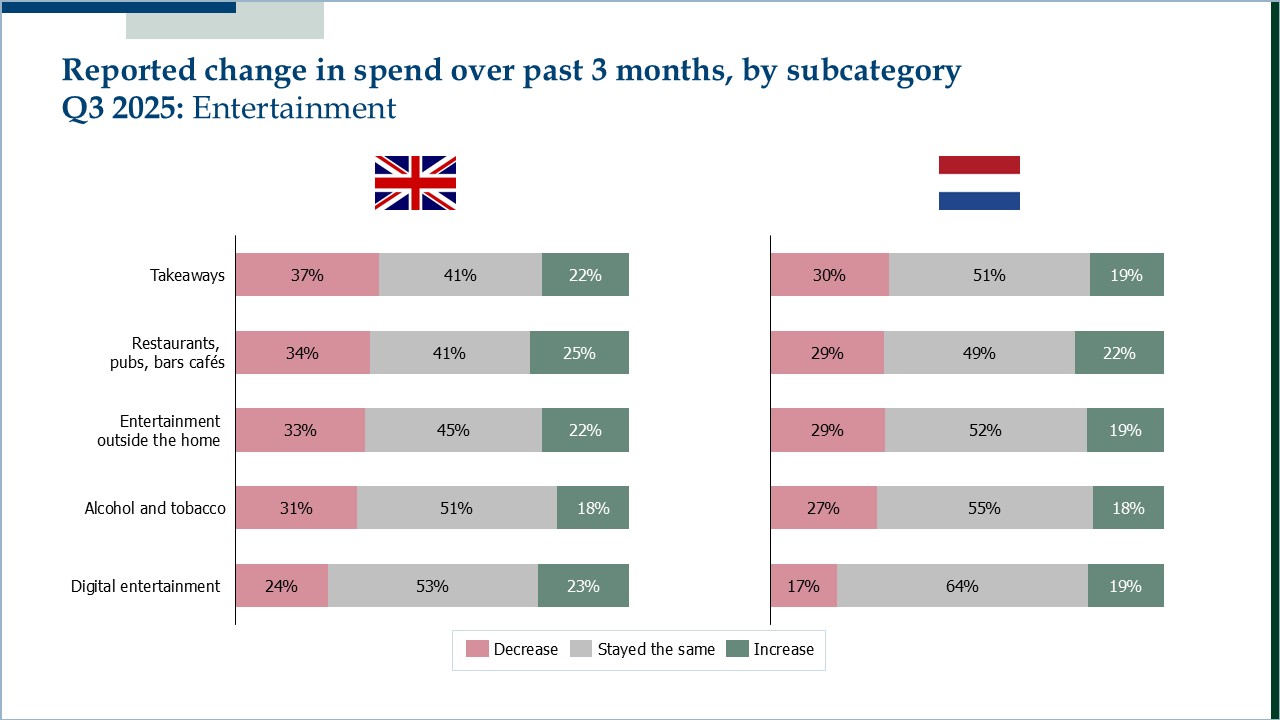

British consumers in particular have also been cutting back on several items under the “entertainment” heading. More have reduced spending than have increased it on takeaway meals, restaurants, entertainment outside the home, and alcohol and tobacco. Only on digital entertainment is there an even balance between those spending more and those spending less. In the Netherlands, there is a similar if slightly less pronounced spending pattern.

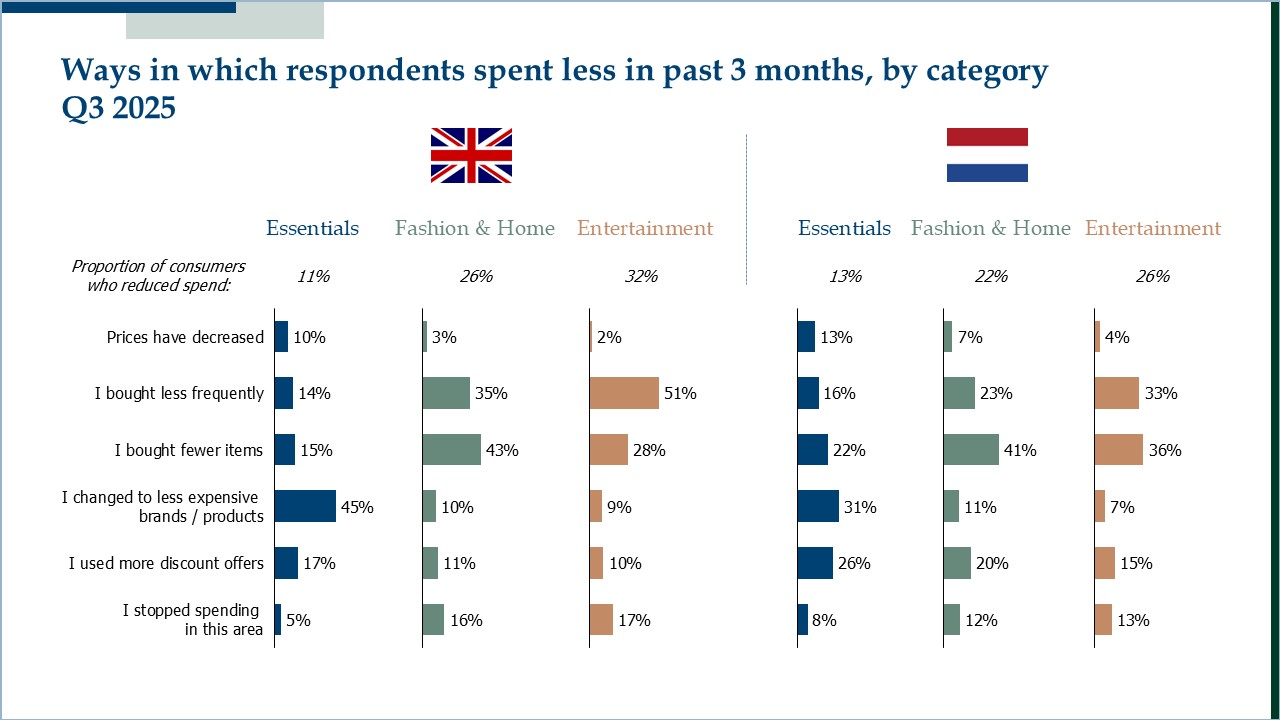

How and why are people spending less?

In the UK the main option for reducing spending in essentials was overwhelmingly to trade down (45% said this). In the Netherlands, consumers who are spending less on essential items are mainly either trading down to less expensive items (31% said this) or using more discount offers (26% said this). 22% bought fewer items. British consumers who are spending less on fashion & home and entertainment mainly did so by buying fewer items and buying less frequently, a similar picture to that seen in the Netherlands (although here too Dutch shoppers are greater users of discount offers, while British shoppers are more inclined to simply cut a product out altogether).

Dena McCallum, co-founder of Eden McCallum, says that continued pressure on spending due to ongoing inflation on essentials means that consumers are more discerning about where they spend their discretionary pounds and euros. Businesses have to be clear about the value proposition of their goods and services. “Consumers are increasingly mindful of price points and the value for money they expect to see,” she says. “There is still consumer demand out there, but also a lot of competition for share of wallet. The winners will be those businesses that deliver genuine value.”

Click here to see the full data for the UK results

Click here to see the full data for the NL results

Follow us on LinkedIn to remain updated