Results of Eden McCallum’s Economic Outlook survey 2014

A small but distinct chill has descended on some UK businesses as they look forward to 2015. The strong optimism of December 2013 has faltered a little, leaving several companies slightly less certain about future business prospects.

That is one conclusion to draw from the second annual Eden McCallum survey of their corporate clients and other businesses. A total of 358 executives responded to a short questionnaire this month providing comparative data on a similar set of questions that were asked this time last year.

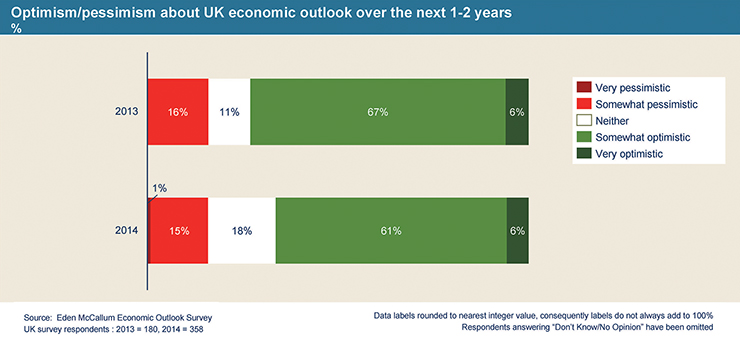

While 67% of respondents are still optimistic about prospects for the UK economy next year, this number is down 6 percentage points on the 2013 figure.

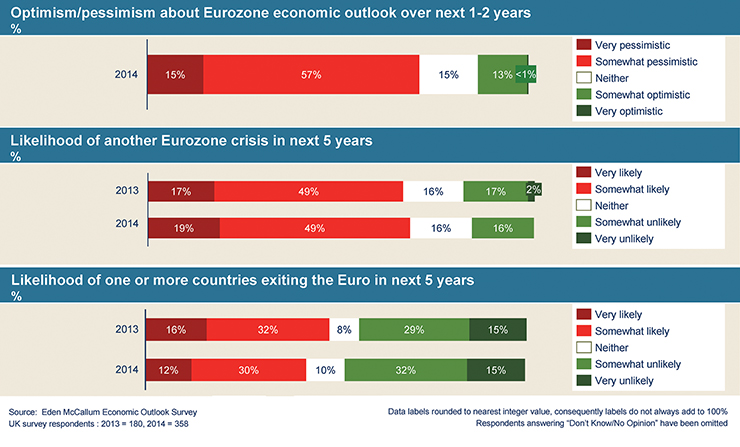

What is causing the concern? There is still nervousness about the Eurozone – 72% are bearish – and two thirds expect another Eurozone crisis in the next five years (unchanged from last year). However, an actual exit from the Eurozone by any country is seen as slightly less likely than a year ago (42% see this as a possibility, down from 48% a year ago).

Adair Turner, senior fellow at the Institute for New Economic Thinking, sees these findings as a realistic assessment of where we stand. “Uncertainty is a natural response,” Lord Turner says. “Even the recent fall in the oil price, which might ordinarily have been seen as good for growth, is having other consequences whose impact may be far less positive. There are strong deflationary headwinds which, in addition to the continuing debt overhang and the difficulties being faced by China as it struggles with the late stages of a credit and property boom, all add up to create an uncertain picture.”

Philip Hanson, products and marketing director at Travelex, the foreign exchange business, says he is not surprised by the findings in this year’s survey.

“These results reflect the contradictory trends which have been evident in the UK for some time now,” he says, “optimism driven largely by micro factors and focused on the UK economy, tempered by pessimism driven by macro factors such as concerns around Europe and China. While respondents are clearly feeling a little more settled about the outlook for the global economy, there are still lingering fears of another financial crisis – which is not surprising, with many people still coming to terms with the trauma of 2008.”

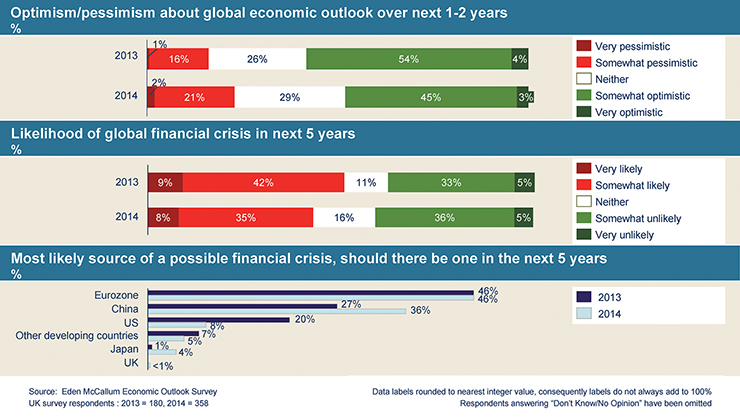

While the survey revealed that there is less optimism about the global economic outlook compared with a year ago (a fall of ten percentage points to 48%), there is also less concern about a global financial crisis (the “fear factor” has fallen eight points to 43%). All the same, there is more nervousness about China as a possible source of future problems (36% now see this as a potential hazard, up from 27% last year). The Eurozone is still seen as the most likely source of a future crisis, however (46% hold this view, as they did last year).

Lord Turner suggests that while policy makers have had an impact in reducing the prospect of another systemic financial crisis, it has proved harder to steer the global economy onto a healthier growth path. As he forecast in a speech at the RSA in London a year ago, the global debt overhang has led to interest rates remaining lower for longer than most then appreciated. This pattern will continue for some time, he believes.

Political risk is clearly a concern, Travelex’s Hanson says. “In this environment of contradictory drivers, it is not surprising that many businesses are focusing on proven strategies, strong propositions and business cases with reliable short-term returns. And just a few are taking a more positive long-term view and placing some big bets for the future, for example in technology.”

Marcus Grubb, managing director for investment strategy at the World Gold Council, also pointed to contradictory forces at work in the global economy. “The falling oil price has a disinflationary effect boosting growth, but this is not necessarily the good news many assume it must be, because it lowers inflation rates at a time when Central Banks are struggling to maintain economic momentum. On the plus side however, there is a risk that interest rate rises will now be put off into the longer term, which is a positive but may not be ideal longer term as asset bubbles will continue to inflate. And yet a lower oil price could lead to possible deflation. It is a paradoxical situation,” he says.

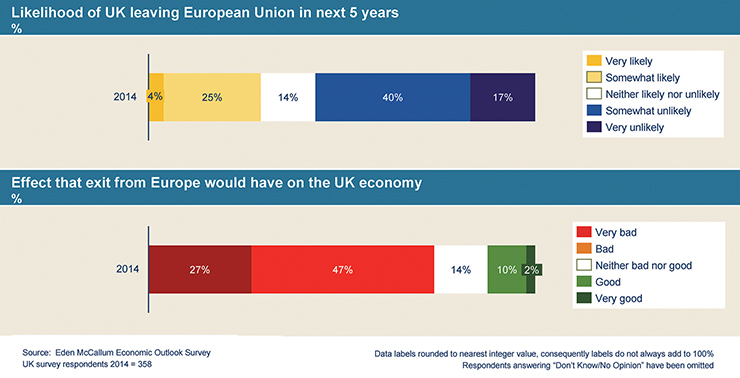

Although the Eurozone is viewed with some caution, most respondents to Eden McCallum’s survey do not expect the UK to leave the EU in the next 5 years. Nearly 30% believe it is likely, while three quarters think an exit would be bad for the UK economy.

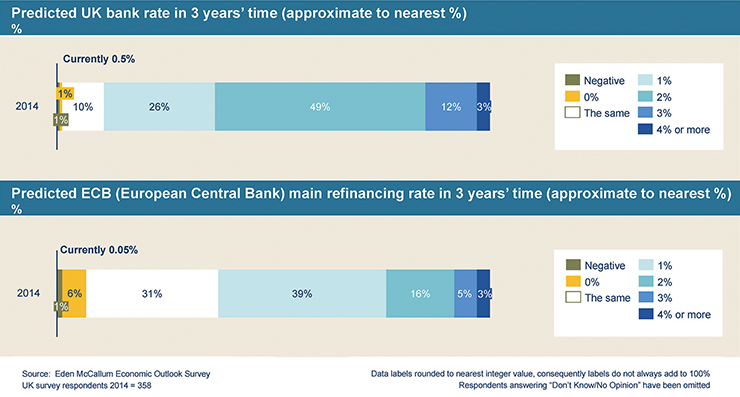

And at least the interest rate environment is expected to remain supportive to growth: most see the UK bank rate rising only to between 1%-2% in three years’ time.

And at least the interest rate environment is expected to remain supportive to growth: most see the UK bank rate rising only to between 1%-2% in three years’ time.

Dena McCallum, co-founder of Eden McCallum, notes “Most of our clients remain cautiously optimistic – the optimism means they are looking at growth strategies, but the caution is leading to a focus on doing a smaller number of things well, rather than placing a lot of bets.”

Eden McCallum’s Economic Outlook Survey

Eden McCallum’s survey was conducted online with their network of clients and other business leaders. Responses were gathered 21-28 November 2014, and at the same time of year in 2013. In 2014 there were 358 respondents to the UK survey. 85% of 2014 respondents were Chairs, CEOs/MDs, Board Directors, divisional Directors, or VP/Partners, within publicly-listed companies (48% of respondents), privately-held companies (48%), state-owned entities (1%) and other types of organisation.