Eden McCallum – Economic and Business Outlook Survey Q2 2026

The latest Eden McCallum economic and business outlook survey has captured what may be a threshold moment, as business leaders look to the future with optimism for their companies, yet acute awareness of daunting uncertainties in geopolitics and technology.

Almost 300 business leaders worldwide were surveyed for their views on the business and economic outlook, with a particular focus on the UK, the Netherlands, and the US. The results tell a story of companies dealing with the impact of the Iran war and adapting to face new and emerging challenges related to shifting consumer demand, technological change (especially AI), supply chain disruption, and commodity price volatility.

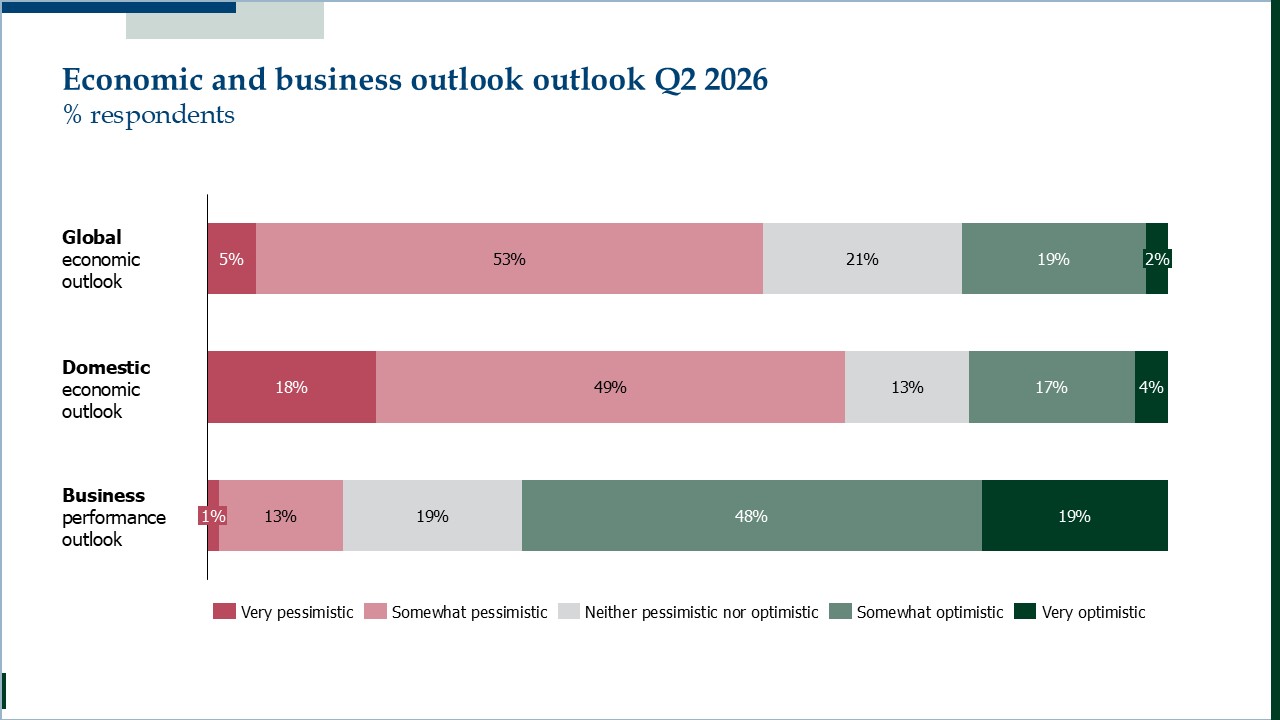

The overall outlook

There is good news and bad news about business sentiment when considering the outlook for the next one to two years. The good news is that, compared with a year ago, there is less pessimism about global prospects. The bad news is that, when last year’s data was being gathered, businesses were still processing the implications of President Trump’s so-called “Liberation Day” – the announcement of severe tariffs on trade. Now, as tariff concerns recede, a new set of external threats is rising to the top of leaders’ minds.

Perhaps surprisingly, as many as 67% of business leaders say they are optimistic about their own company’s prospects, up from 52% a year ago (but down from the 71% who felt positive in Q2 in 2023 and 2024). As far as the global and domestic economy is concerned, however, there is much more gloom: 58% are pessimistic about the global economy and 67% are pessimistic about the domestic economy. Admittedly, business leaders were even less hopeful about the global economy and their own business’s prospects a year ago.

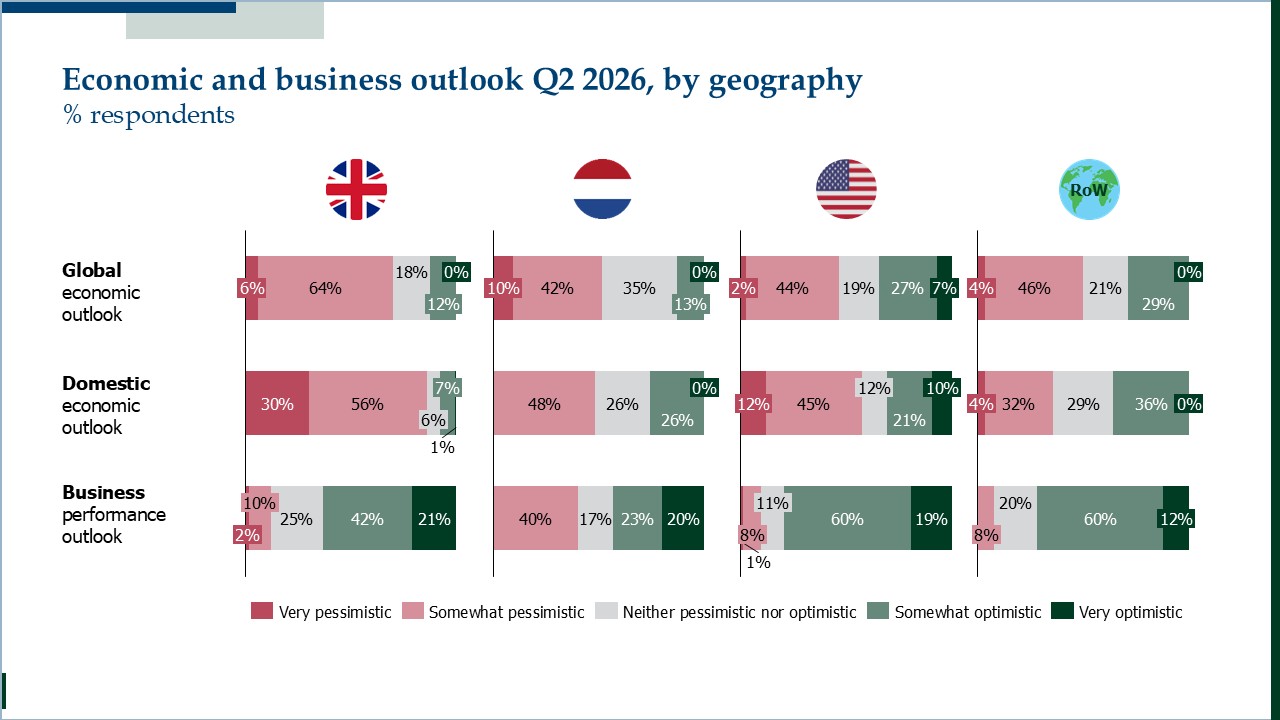

UK business leaders stand out for their levels of pessimism about their home market: 86% are gloomy. The Dutch are the least bullish about their own businesses’ prospects, with 40% who are pessimistic balanced against the 43% who are optimistic. In the US, 8 out of 10 business leaders are optimistic about their own company’s future.

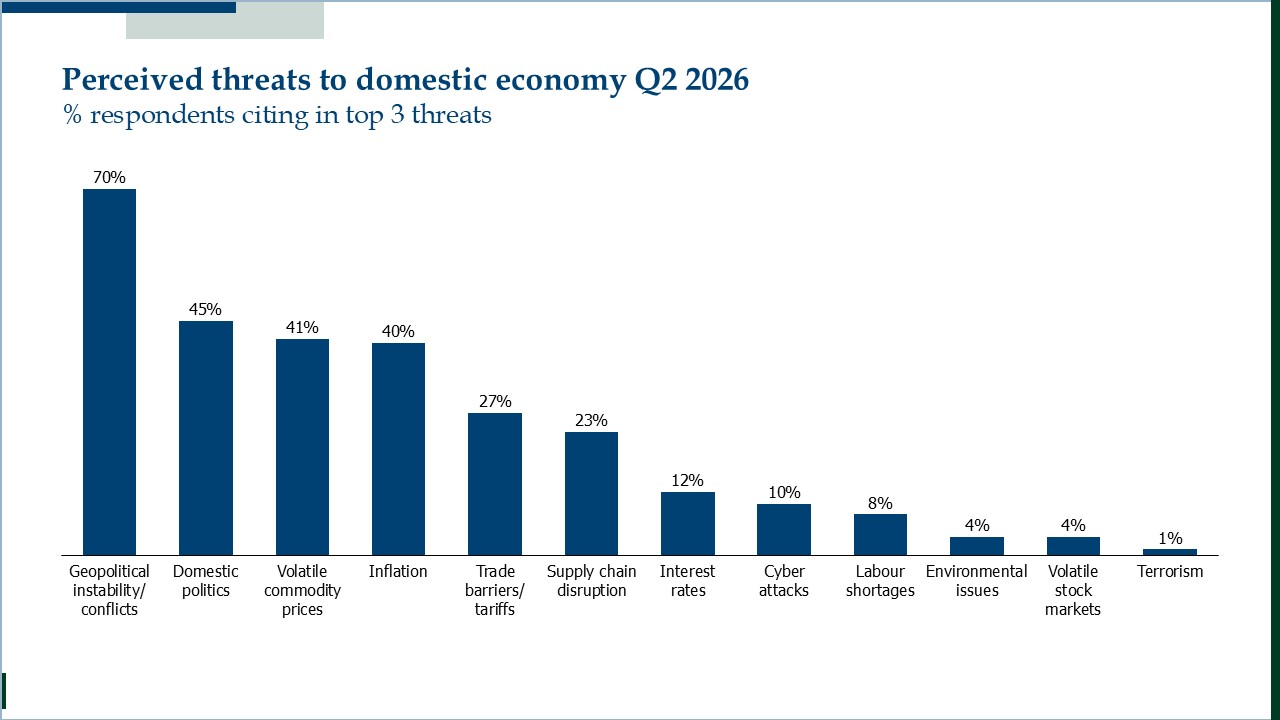

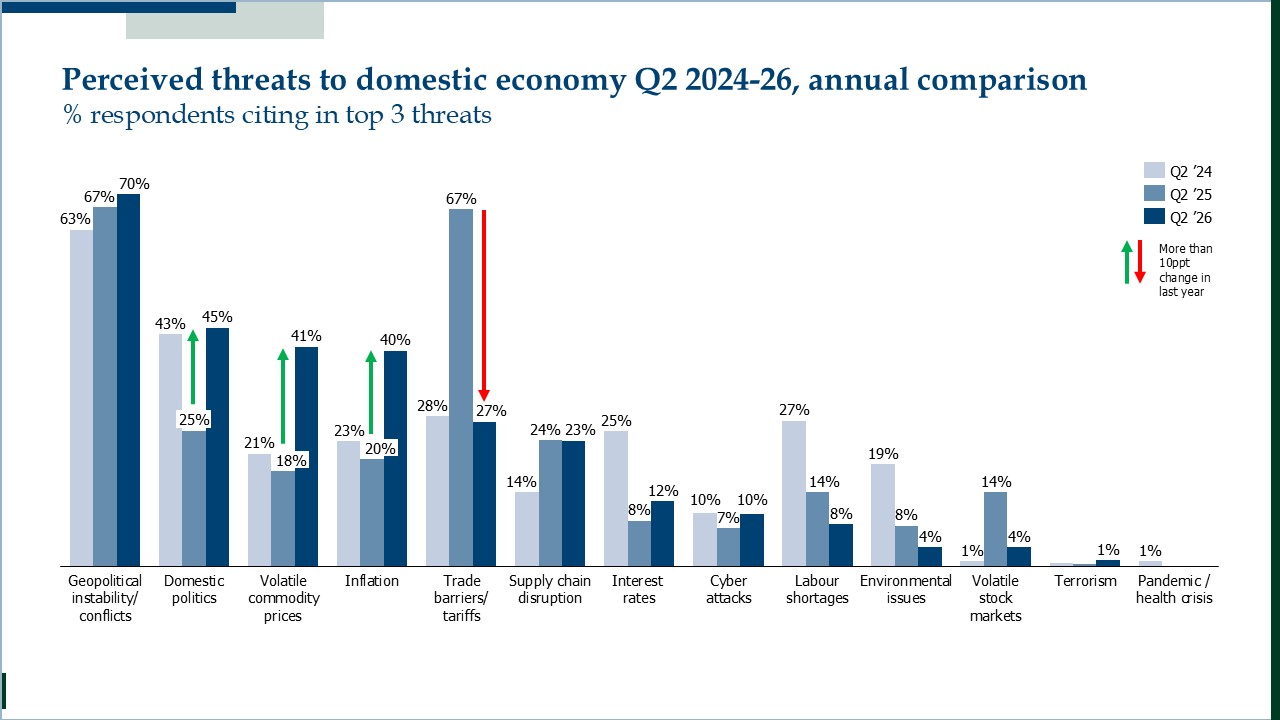

Threats

As far as threats to respondents’ domestic economy are concerned, geopolitical instability is seen as by far the biggest potential problem: 70% named it among the three greatest threats. Around 40% cited domestic politics, volatile commodity prices and inflation. Interestingly, a year on from “Liberation Day”, only 27% see trade barriers and tariffs among the greatest threats (vs 67% a year ago), while 23% fear supply chain disruption.

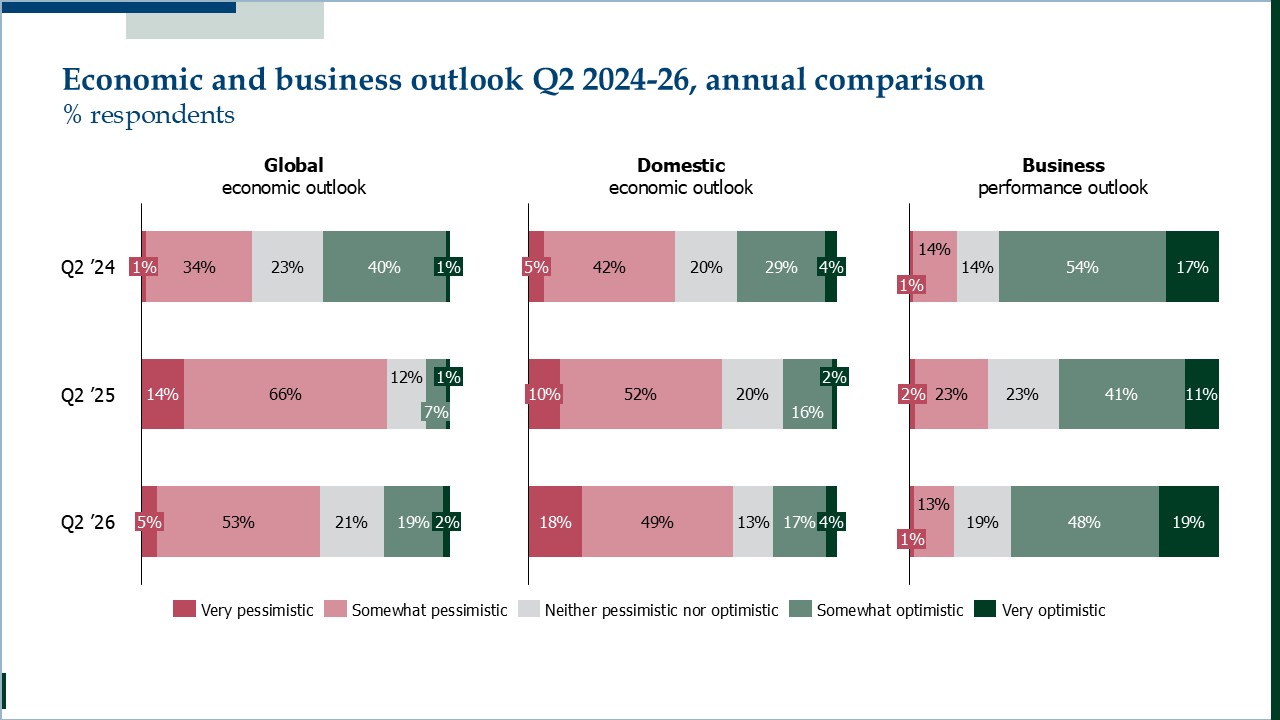

What a difference a year makes

Changes in the perception of threats have been quite dramatic over the past 12 months. The concern over domestic politics, commodity price volatility and inflation all rose sharply to roughly double the level it had been in Q2 2025, while concern over trade barriers / tariffs has more than halved. Geopolitical instability has remained a top threat throughout.

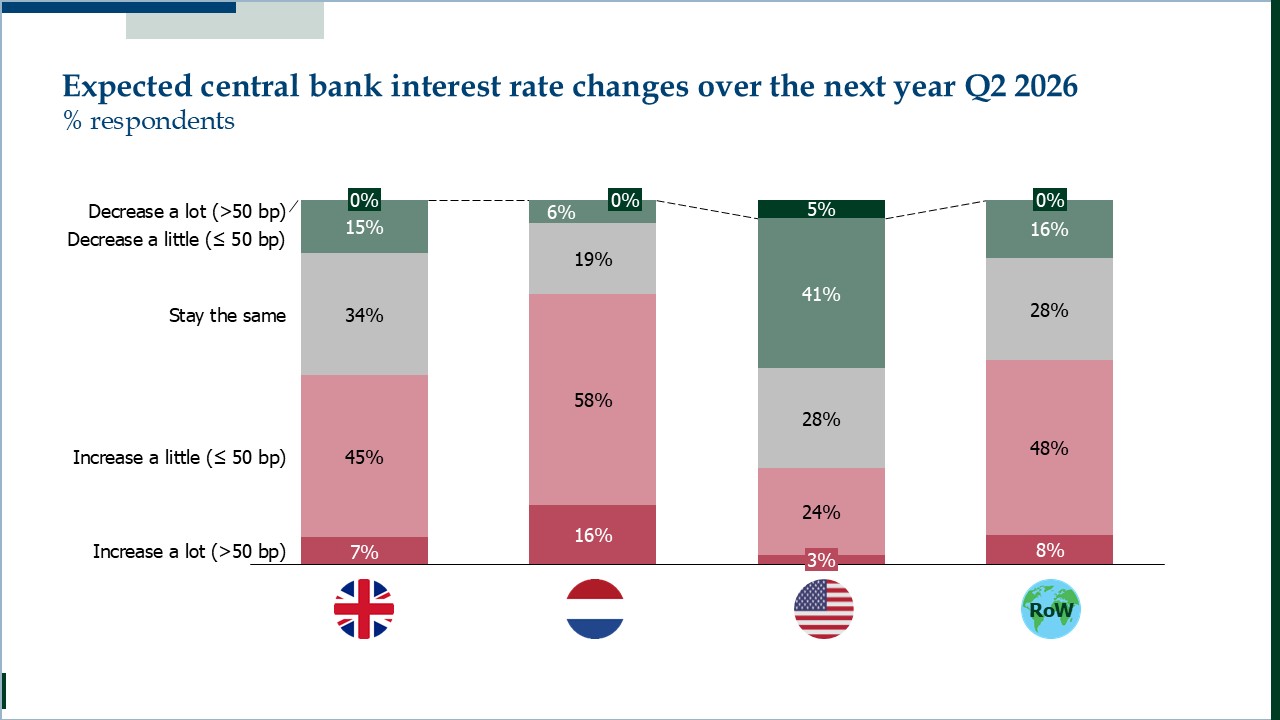

Interest rates and inflation

There are differing perspectives on the prospects for interest rate movements over the next couple of years. About half of business leaders expect interest rates to increase over the next year. That proportion rises to 74% in the Netherlands, while in the US 46% expect to see a drop in rates (with only 27% expecting rates to rise), perhaps a sign that the incoming chair of the Federal Reserve, Kevin Warsh, is expected to be more receptive to pressure from President Trump to reduce rates.

But overall, concern internationally about interest rate rises is up sharply over the last two years.

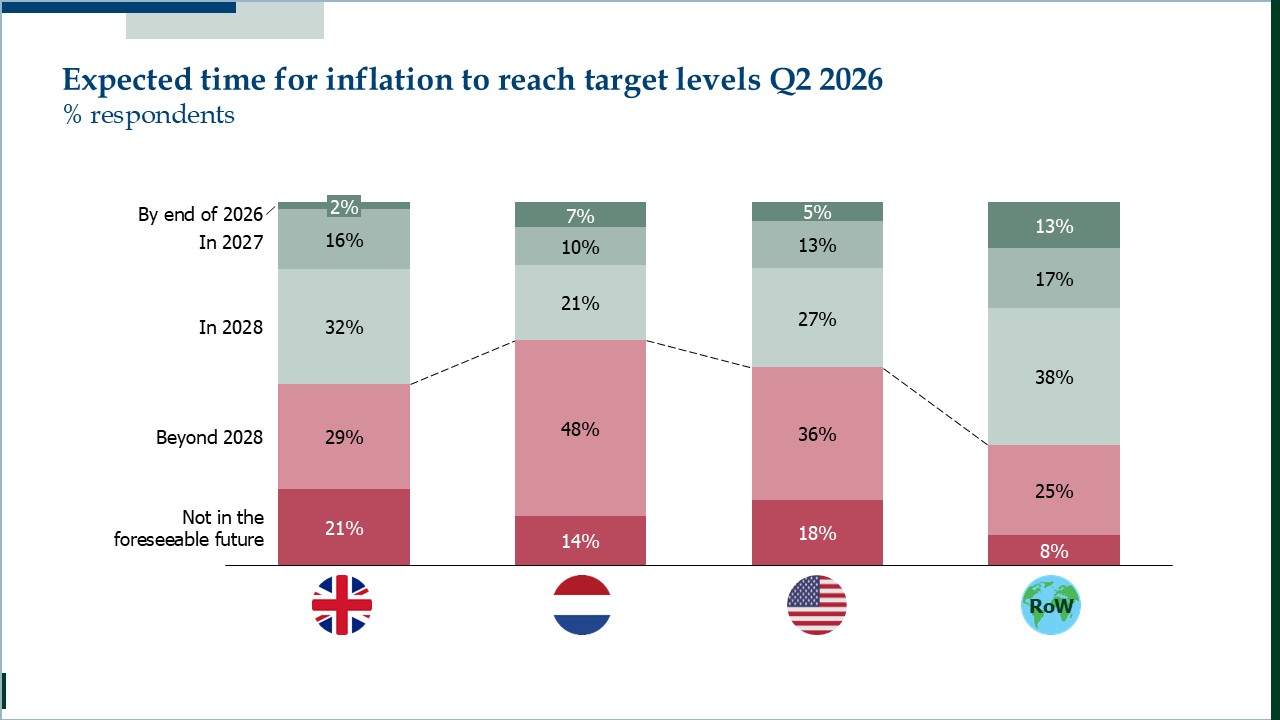

Just under half of business leaders expect inflation to reach its target 2% level by the end of 2028. Dutch business leaders are the most pessimistic on this point: 62% do not think inflation will be on target by then.

Both British and Dutch business leaders have become more pessimistic about inflation in the past two years. That trend is especially pronounced in the Netherlands.

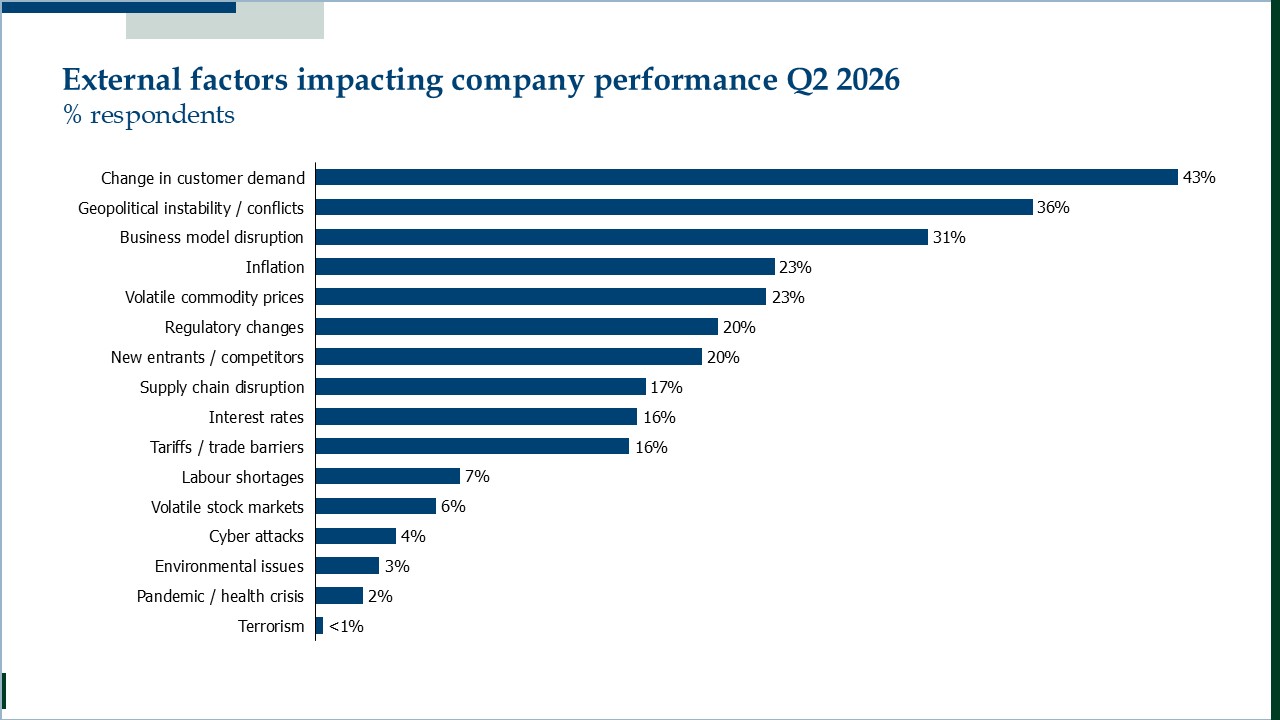

The business outlook

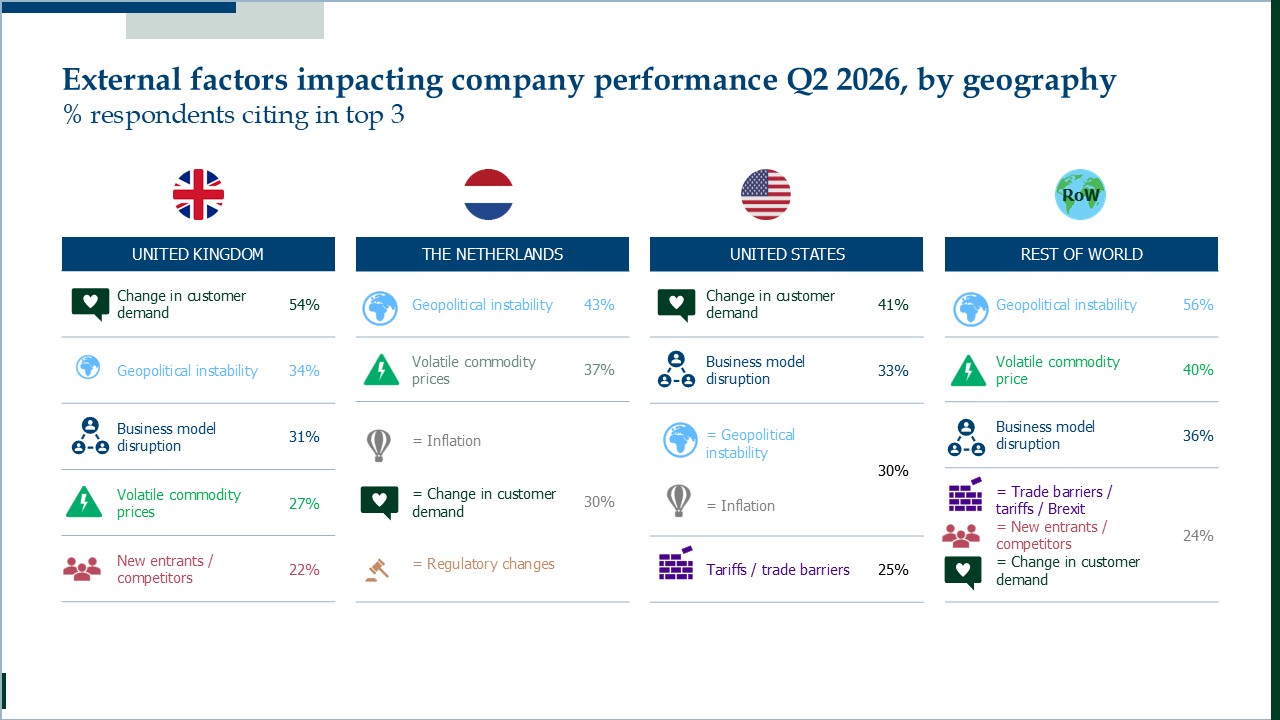

Optimism about business performance has recovered after a dip last year. The three external factors seen as most likely to have an impact on business performance are changing customer demand (cited by 43%), followed by geopolitical instability (36%) and business model disruption (31%). Inflation and volatile commodity prices are also mentioned by 23% of respondents.

Business leaders in the UK and US are most concerned about customer demand while Dutch and other European leaders are most exercised about geopolitical instability.

Business model disruption and volatile commodity prices have risen in importance in the last year, while concern about tariffs/trade barriers and volatile stock markets has declined. But the top two areas of concern have consistently been changing customer demand and geopolitics.

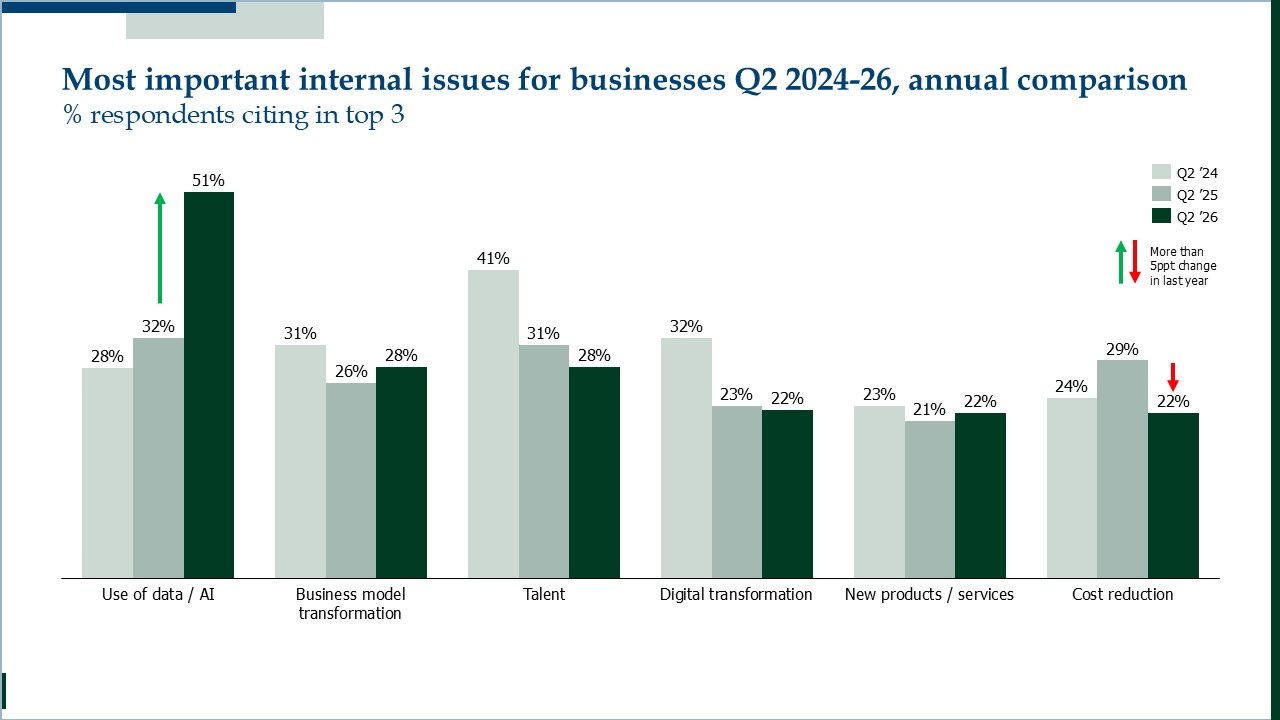

Use of data and AI

As far as internal issues are concerned, optimising data and AI has risen sharply in importance over the last year and is now the leading priority – 51% of respondents say it is in their top three internal issues. Business model transformation and talent are the next most-cited top issues, mentioned by 28%. Until last year, talent had been the leading issue since Covid, so it is notable that AI has usurped it so strongly.

Current turmoil

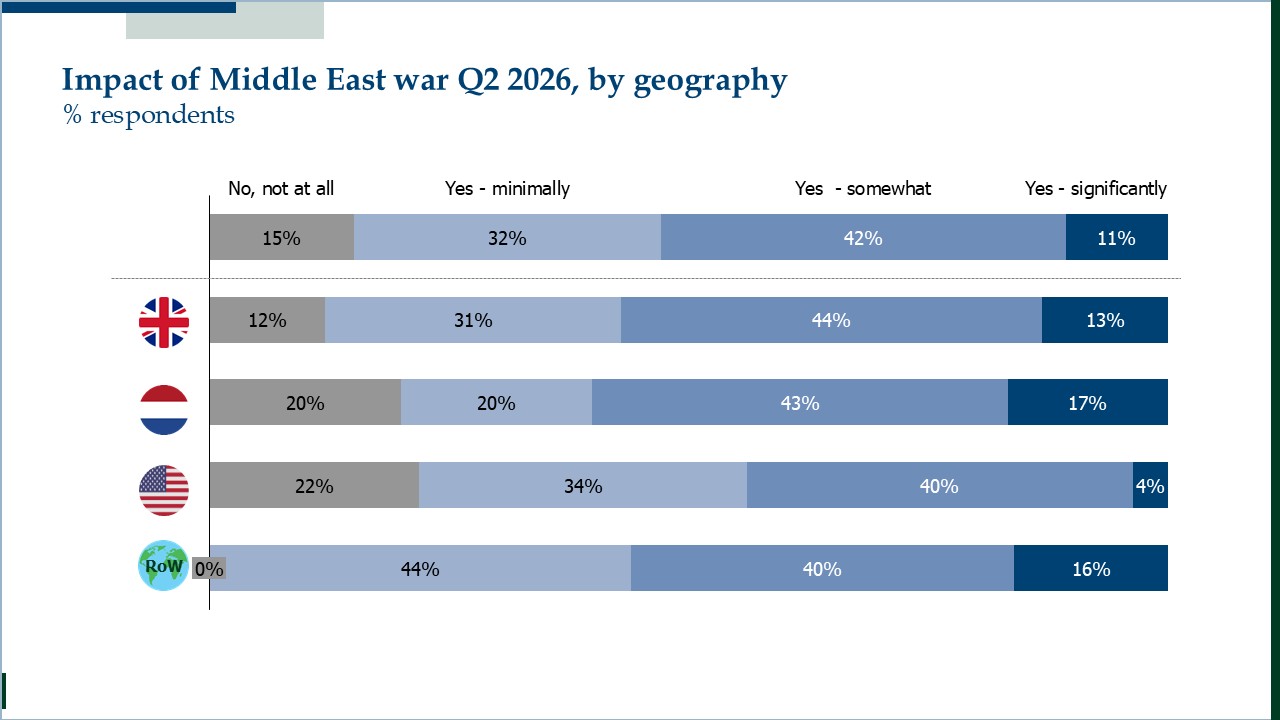

When asked specifically about the impact of the war in the Middle East, 85% of business leaders say it is having some impact on their company. Businesses in the UK, Netherlands and the rest of the world have felt a greater impact than those in the US.

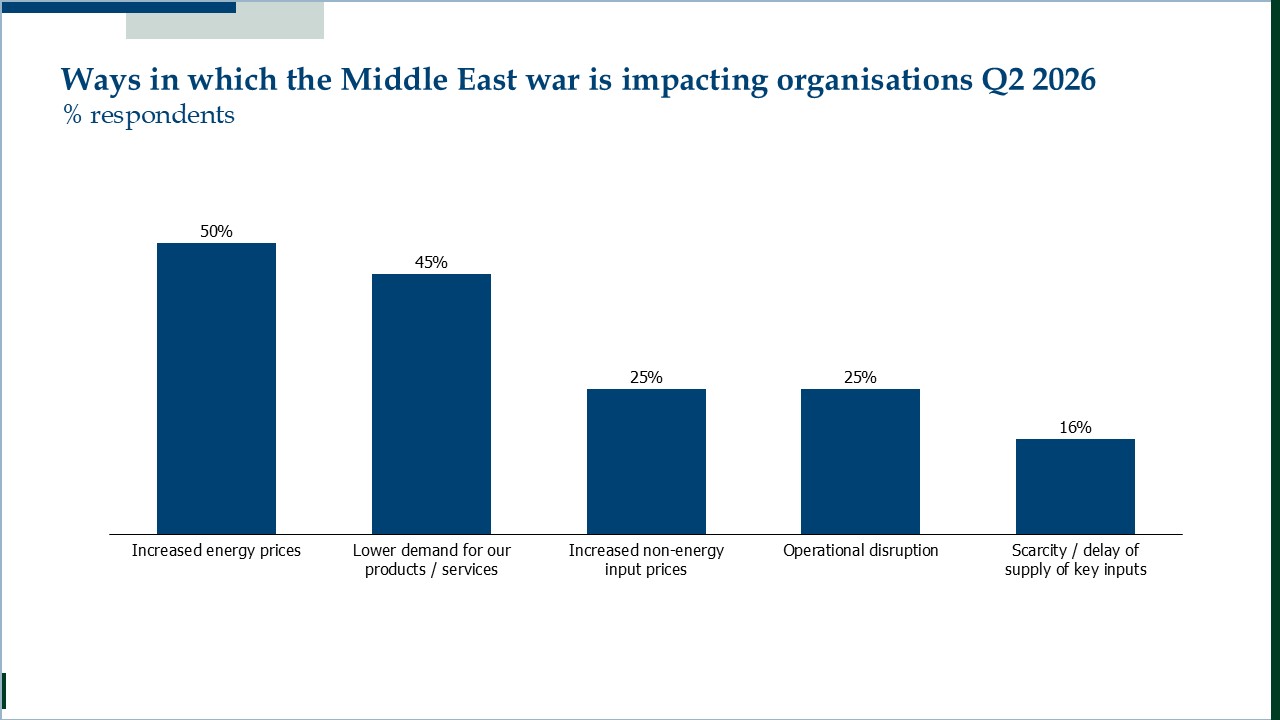

An increased cost of energy is the most prevalent way in which the war has had an impact (50% of business leaders mention this), while lower demand for products and services was cited by 45%.

Dena McCallum, co-founder of Eden McCallum, says that leaders are adapting quickly to such volatility – and perhaps becoming slightly anaesthetised to it. “Despite the rapidly rising uncertainties from both geopolitics and AI, business leaders are responding with agility and optimism for their companies’ prospects.” That said, concerns for the economy are high (although not as high as they were a year ago), and “it may be that the real turbulence has yet to be felt.”

Click here for the full survey results.

Follow us on LinkedIn to remain updated.

*Eden McCallum’s semi-annual Economic and Business Outlook Survey was conducted from 17 to 24 April 2026 and in conjunction with HighPoint Associates.