Eden McCallum Consumer Sentiment Survey Q3 2025 – Digital purchasing behaviours

Five years on from the days of Covid lockdowns, consumer behaviour, both on- and offline, has shifted and recalibrated. Online penetration has stabilised, after post-Covid declines, for most consumer goods categories and is rising again in some; and in financial services and travel, online penetration continues to grow gradually for purchases, but for customer service in most of these service categories (as well as utilities), the phone is still the dominant channel.

These are the central findings from Eden McCallum’s latest survey of digital consumer behaviour. Around 1,500 consumers in both the UK and the Netherlands were asked to reflect on their spending decisions over the past three months. The survey considered the purchase of physical goods as well as of services, and related customer service. Physical goods included large and small grocery shops, as well as entertainment (e.g., books), electronics, fashion, children’s toys/games, sport/leisure, furniture/home and beauty/personal care. Services included holiday travel and accommodation, financial services (current account, credit card, insurance) and utilities (telecoms and energy).

Digital purchasing of goods still behind 2021 peaks

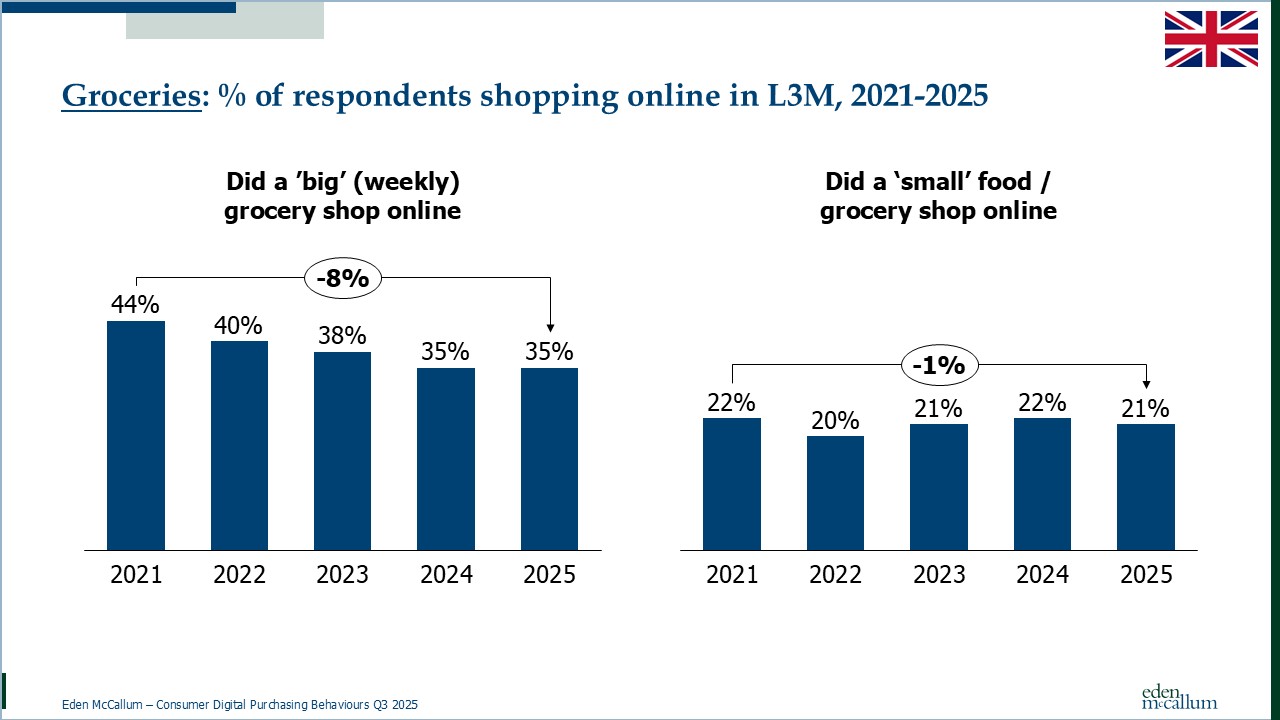

For British consumers the appeal of the big weekly online grocery shop has stopped its post-Covid decline, steadying at c. 35%, vs 44% in 2021. The appeal of doing a small grocery shop online has remained steady at c. 21% over this period.

In the Netherlands, the big weekly shop is now purchased online by 25%, up slightly on the past two years but below the 28% who went for that option in 2021. As in the UK, the small online shop has maintained a steady level of support, in this case at around 18%.

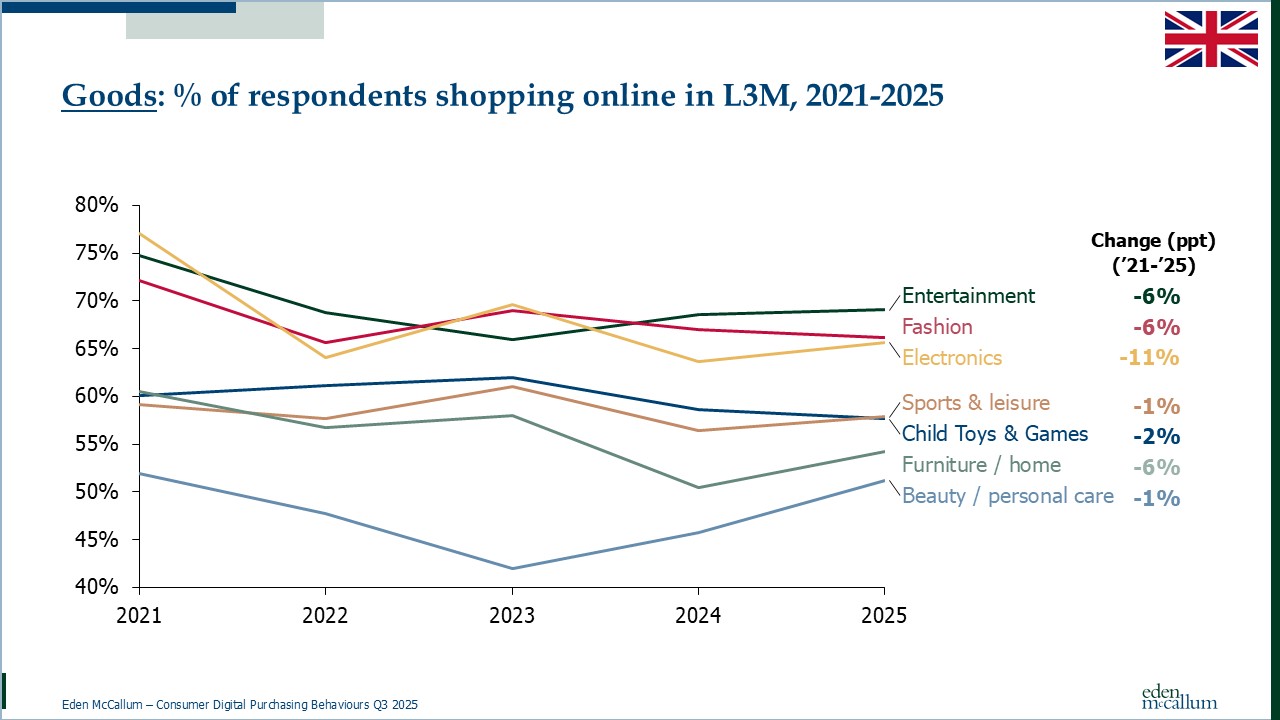

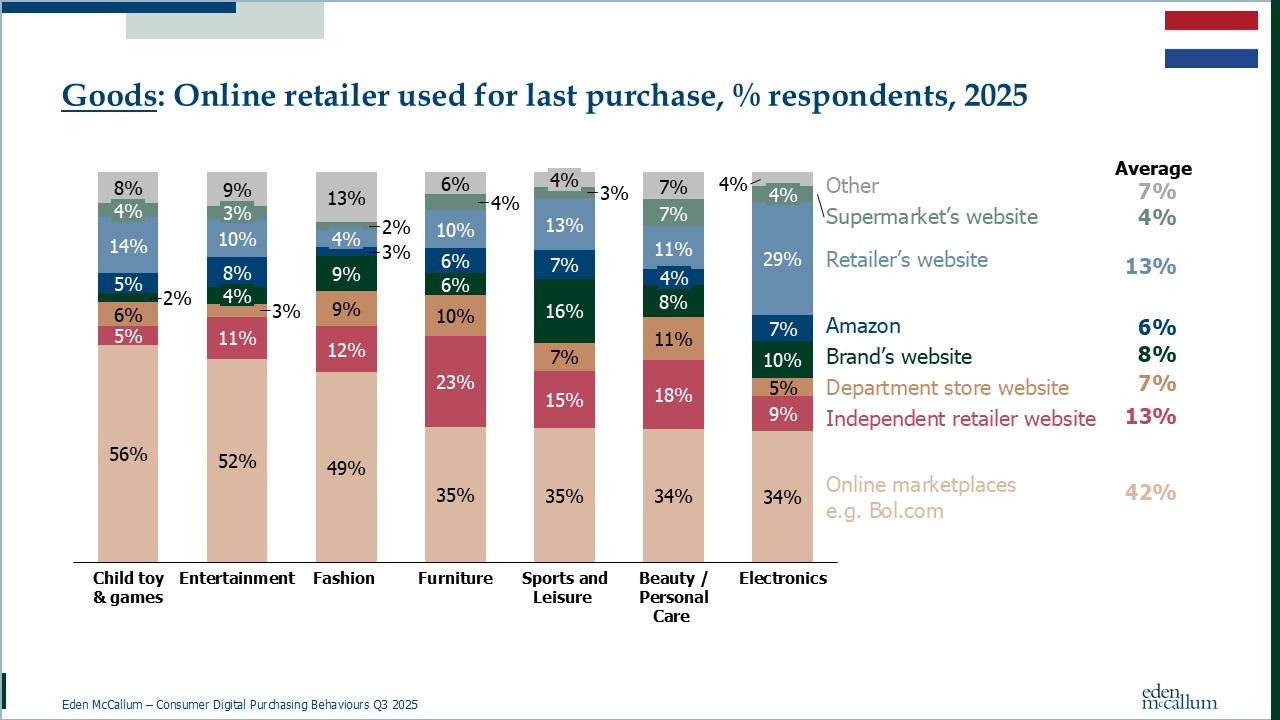

In terms of other physical consumer goods, in the UK, of those who purchased in the last three months, at least half did so online, with entertainment highest (c. 7 in 10) and beauty/personal care lowest (c. 51%). And while online purchasing in all categories was less widespread than in 2021, the declines have flattened for most goods, and in some categories there has been significant growth over the past 1-2 years (e.g., beauty/personal care and furniture/home).

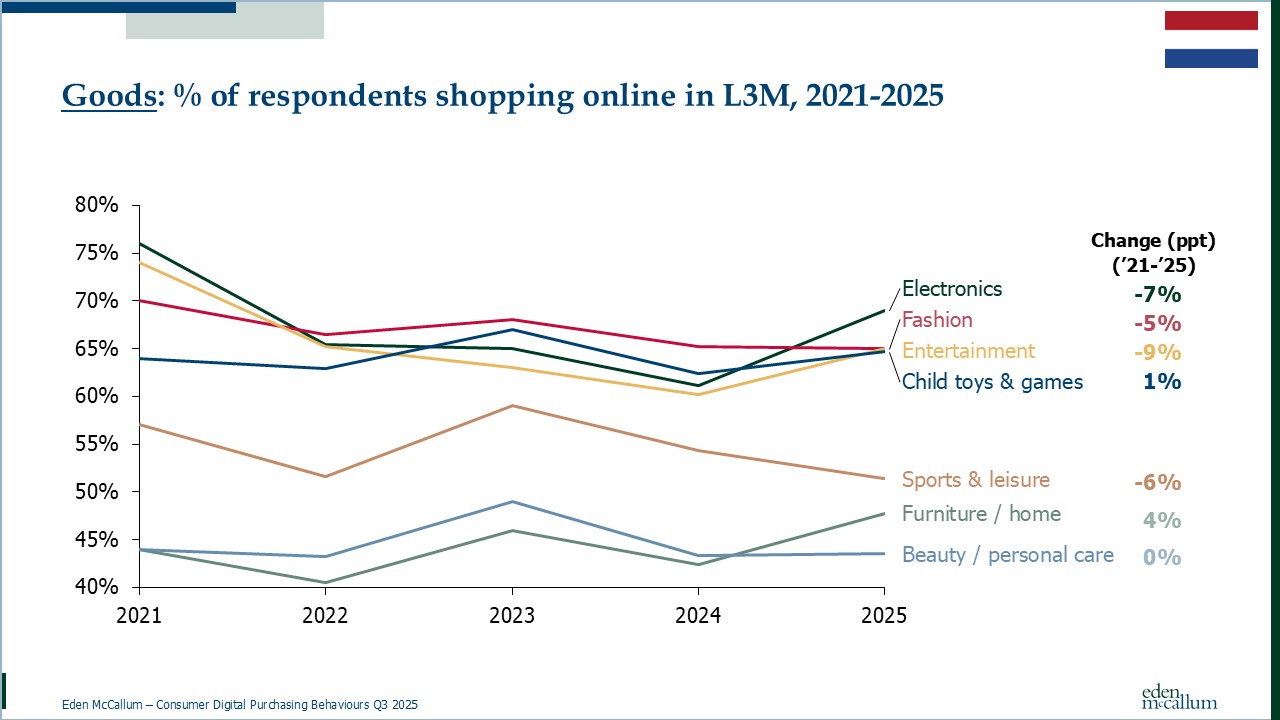

The pattern of spending behaviour has been less predictable in the Netherlands. While penetration of online purchasing in many categories has declined since Covid highs, in furniture/home online purchasing levels are higher, and in children’s toys and beauty/personal care, they are similar. Year on year, there was growth in a number of categories, notably electronics, furniture/home, and entertainment.

In services, online dominance and steady growth

In both countries, those using online channels for holiday bookings (accommodation and travel) have increased since 2021, with around 80% in both markets now favouring this option.

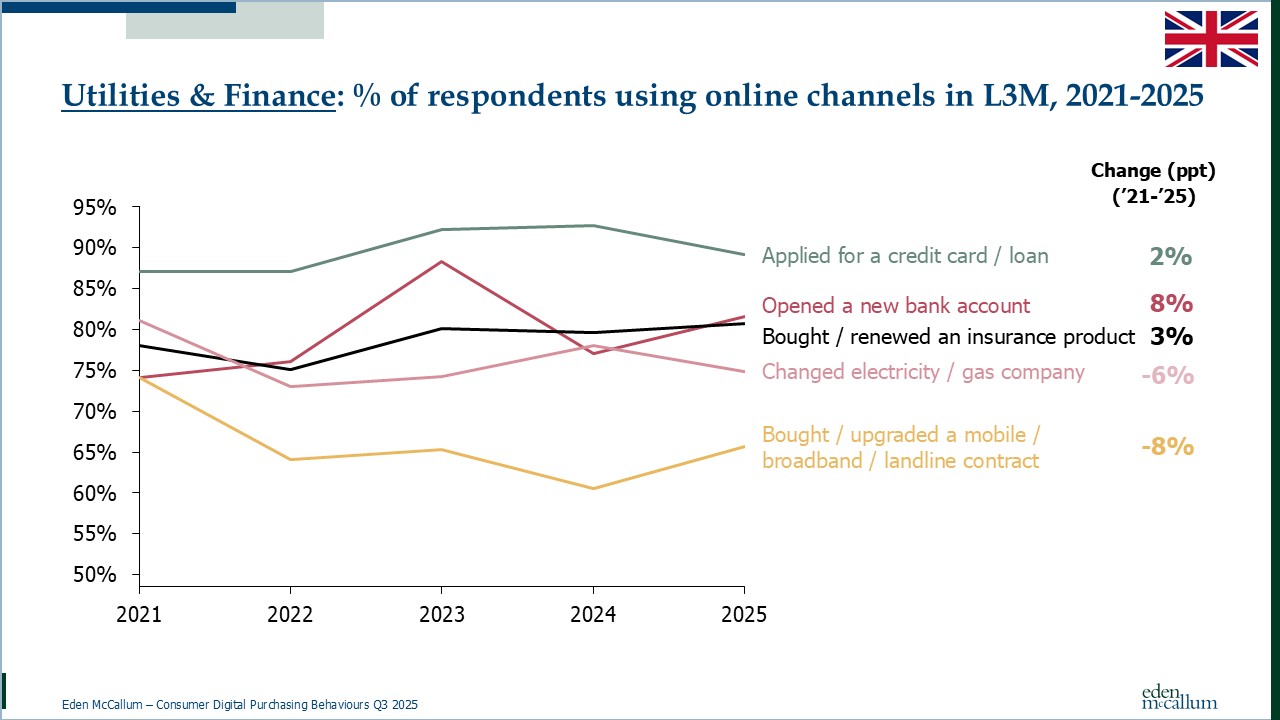

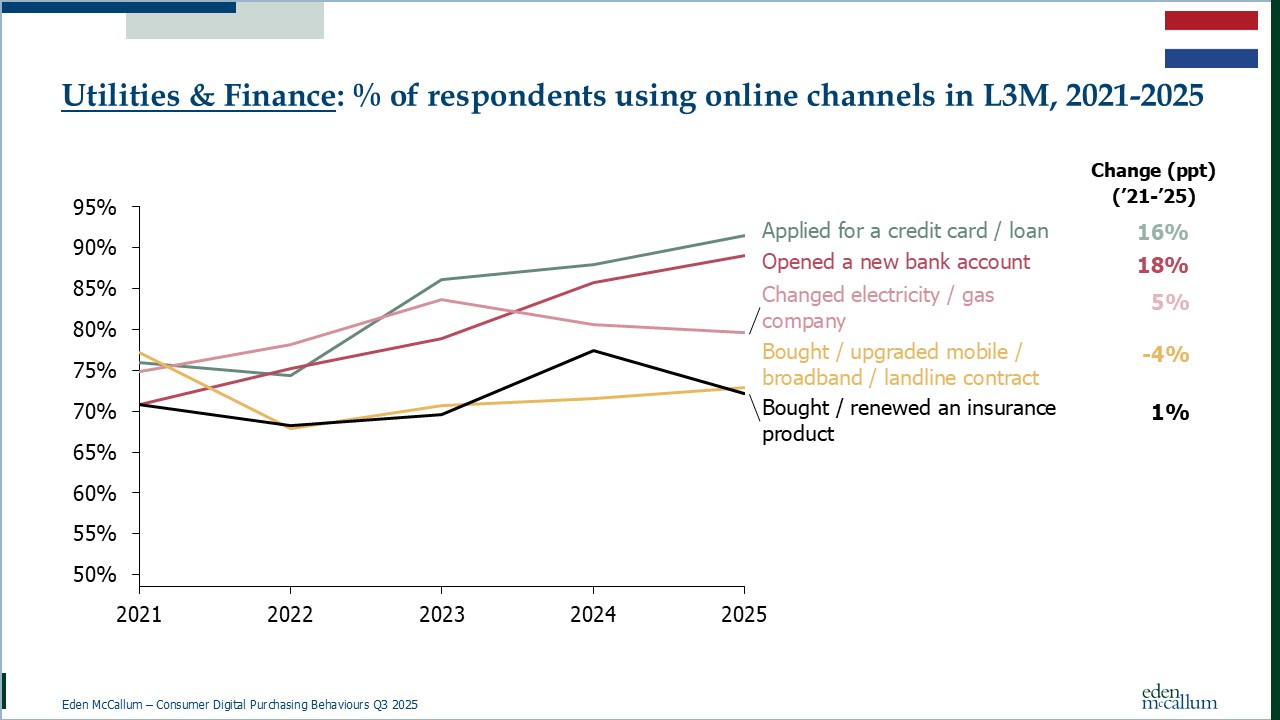

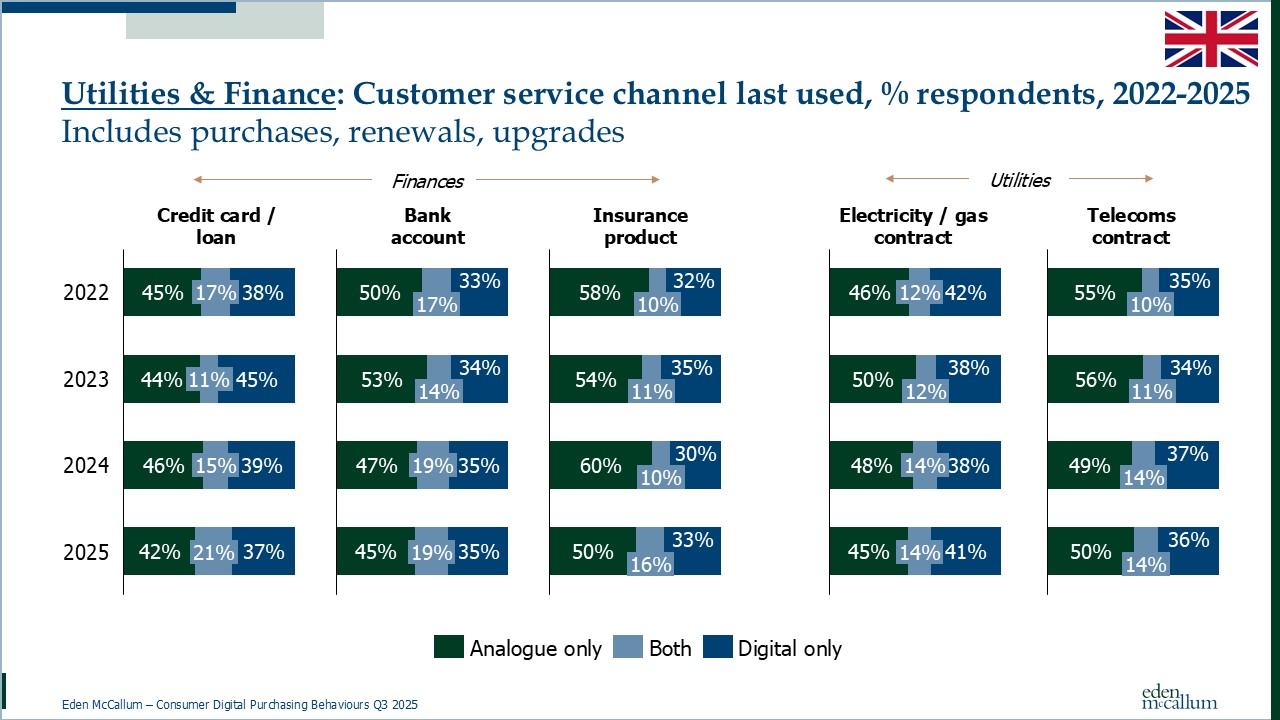

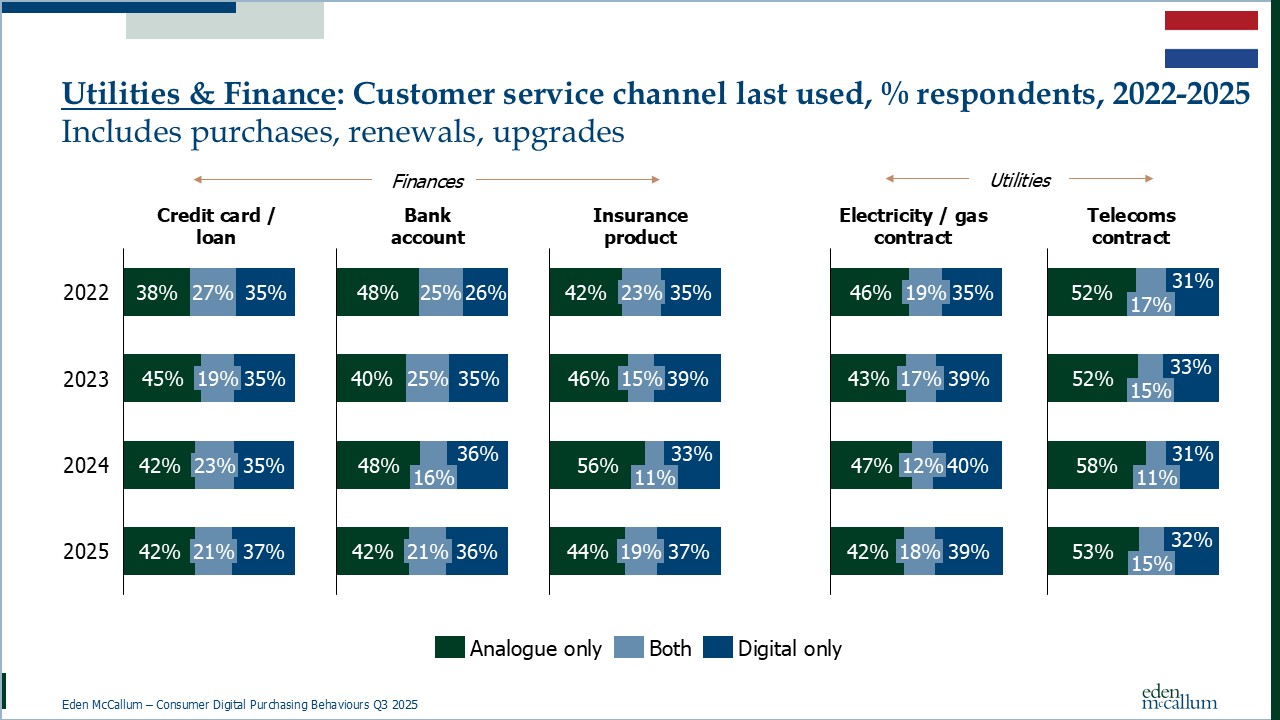

In terms of utilities (telco, energy) and financial services, in both the UK and Netherlands at least 7 in 10 respondents have signed up online for new household utilities contracts or finance products, for example applying for a new credit card or loan or opening a new bank account.

In the UK since 2021, the use of online channels for financial services has increased, whereas for utilities the prevalence of online has declined.

In the Netherlands, on the other hand, online channels have increasingly been used for buying, renewing or upgrading energy contracts and financial services over the last four years. Only mobile/broadband contracts have seen a fall in the share of online purchasing since a 2021 peak.

Why shop online, and where?

In both countries, ease of home delivery is by far the main reason for respondents choosing to buy groceries online: around 70% cite this as far as a big shop is concerned, and over 50% say the same for a smaller shop.

In the UK almost 90% of respondents use supermarket websites for large online grocery shopping, and 70% for smaller shops, with Amazon and Deliveroo / Uber Eats also popular for more modest shopping needs. In the Netherlands supermarket websites are similarly, if not quite so overwhelmingly, popular.

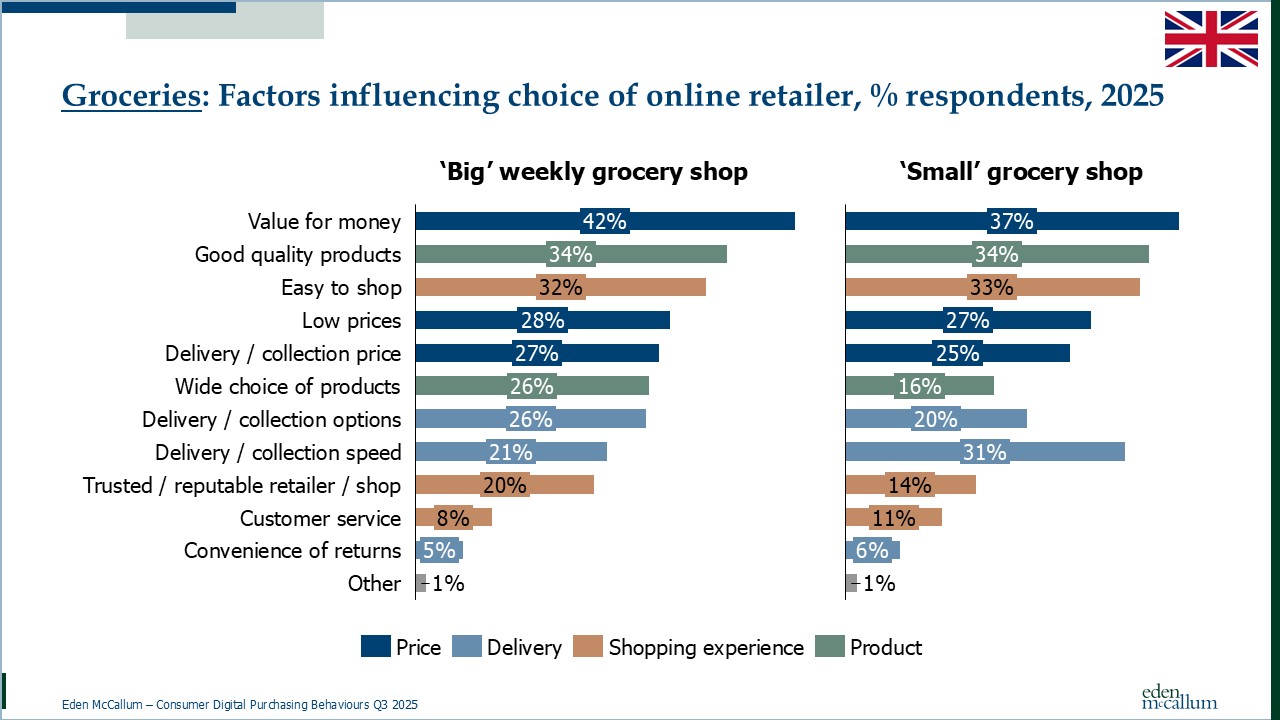

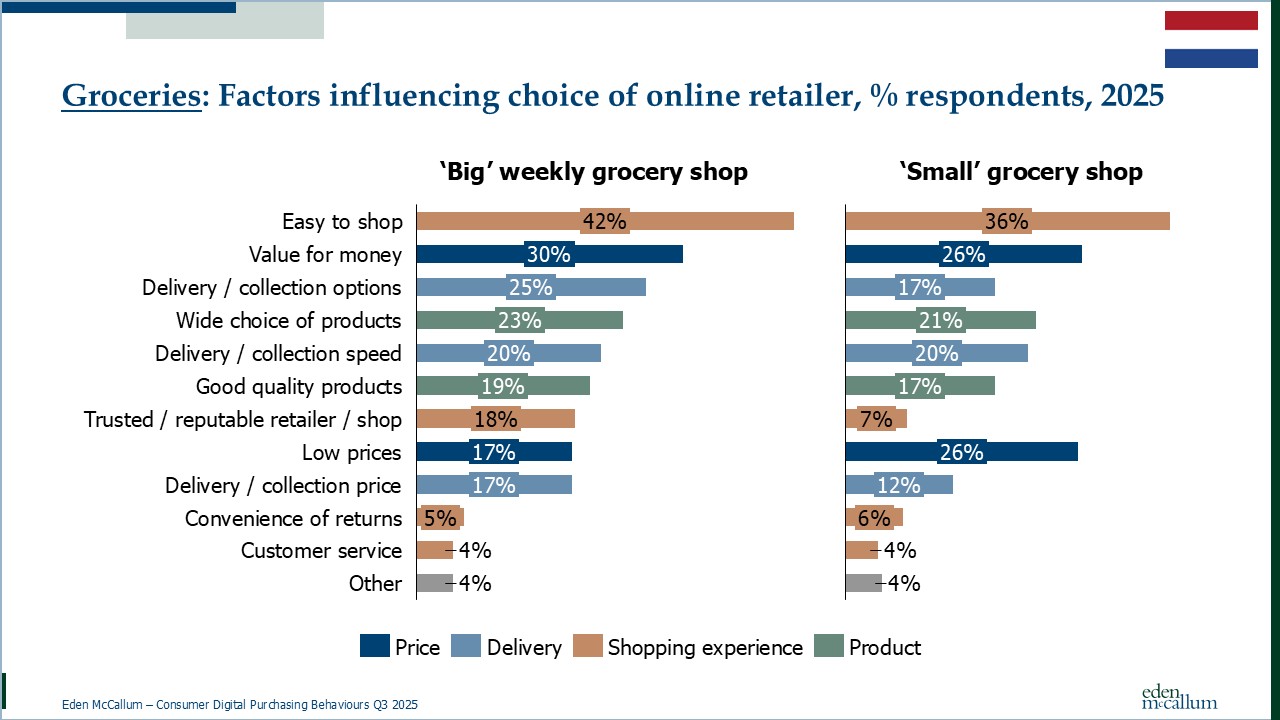

In the UK, value for money and quality are the top factors for respondents when choosing retailers for both big weekly and small grocery shops. In the Netherlands the factors that influence the choice of online grocery retailers are different for big and small shops, although ease and value are important for both. Dutch shoppers also believe they can find lower prices when carrying out their smaller shops (26% say so), while in the UK, delivery speed is a key factor in the choice for smaller grocery shops.

When it comes to other consumer goods, in the UK ease of home delivery is the top reason to shop online (43% say so), closely followed by cheaper prices (39%) and better product choices (32%). In the Netherlands better deals are most important (according to 39% of respondents), while easier home delivery (37%) and product choice (34%) are the other main reasons for respondents to shop online. The differences between categories are surprisingly small.

In the UK, for non-grocery items, value for money (48% cite this) and good quality products (42%) are the most important factors when choosing an online retailer. In the Netherlands value for money (39%), choice (37%) and ease (32%) are the main relevant factors when choosing where to shop online.

Not just Amazon…

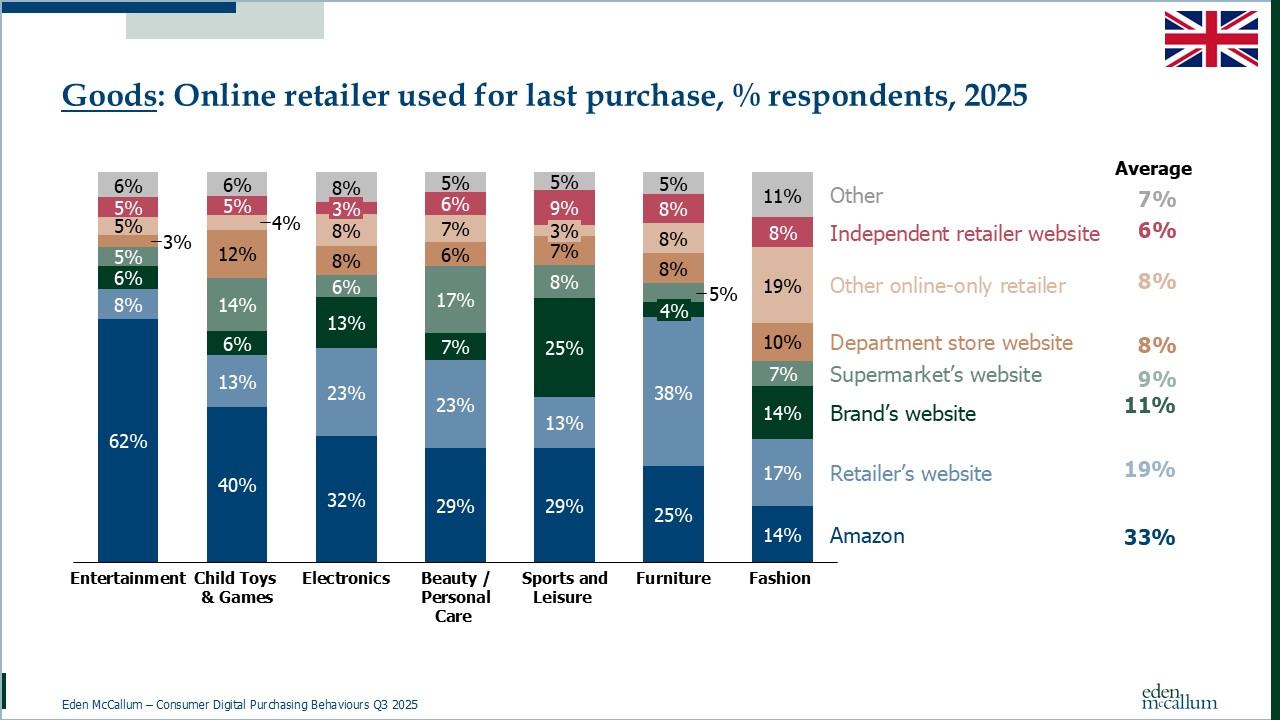

The Netherlands is a rare market where Amazon has not come to dominate online shopping. Other online-only retailers and marketplaces, such as Bol.com, are most popular for purchasing physical goods across all categories. But in the UK, Amazon is the leading retailer for purchasing physical goods online. It is the most popular option in five out of seven categories, with other options preferred for fashion and furniture/home.

Online preferences for services

In both countries, when customers are making travel plans, cheaper deals, ease of comparison and better choice are the main reasons respondents choose to book travel and accommodation online; and for accommodation, the ability to check reviews is also a key factor.

Customers have distinct reasons for going online to purchase financial services and utilities contracts. In the UK, respondents open/apply for bank accounts and credit cards online for convenience (and credit cards also for the best deals); household utilities and insurance to make price comparisons and find deals; and telecoms contracts for speed (as well as better deals). It is a similar story in the Netherlands. Convenience related factors, followed by price and ease of comparing products, are the main reasons respondents choose to handle finance and household utilities online.

But in spite of this widespread online sophistication and maturity, when it comes to utilities and finance-related customer service, UK and Dutch respondents mainly prefer to use analogue channels, particularly the phone, to contact their provider.

In summary, while online usage since Covid for goods has largely declined, it is now stabilising, and in many categories starting to grow again, while for travel and financial services, the usage of online channels has continued to increase since Covid. The sticky exception is for customer service, where analogue channels, particularly the phone, remain dominant. Dena McCallum, co-founder of Eden McCallum, observes “For businesses trying to reduce their contact centre costs, this is a challenge, which generative AI may help to solve. But for now, when things go wrong, people still like talking to a human.”

Click here to see the full data for the UK results

Click here to see the full data for the NL results

Follow us on LinkedIn to remain updated