Economic and Business Outlook Survey: Q2 2023

An uncertain economic environment in which business leaders increasingly expect something better to emerge: that is one way to summarise the findings of the latest Eden McCallum survey of business sentiment. Over 200 business leaders in the UK, the Netherlands and around the world were asked for their views on the state of the economy and their own corporate prospects.

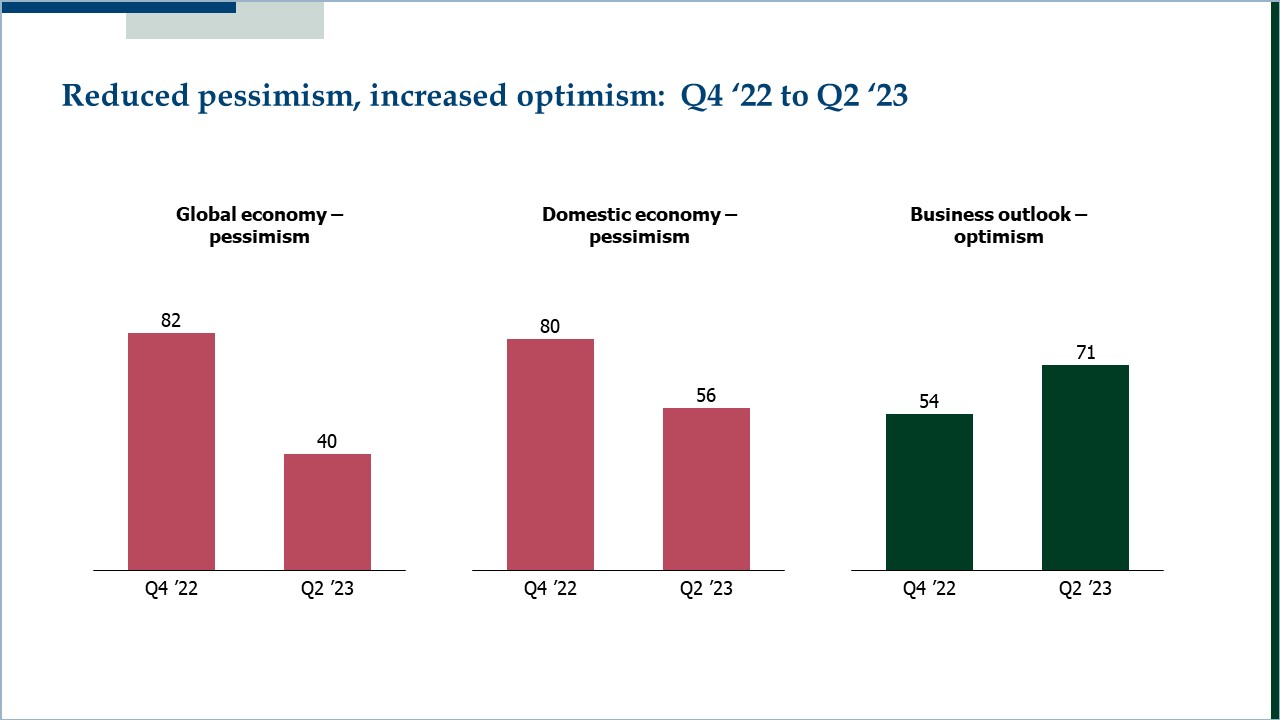

While there has not been a big upsurge in optimism over the past quarter, the outlook has continued to improved. There is still fairly entrenched pessimism about macroeconomic prospects – 40% are still gloomy about the world outlook, and 56% are pessimistic about their domestic economy. And yet 71% are positive about their own business’s future. Indeed, pessimism levels have fallen significantly over the last six months: 82% were pessimistic about the global economy in Q4 2022, and 80% were pessimistic about their domestic economy at that time.

Breaking down the international response by country, it seems that business leaders in the UK and North America are more pessimistic about their domestic economic outlook than their European counterparts. But UK business leaders, while they are the most pessimistic of all about their domestic economy, are growing more optimistic about their company’s performance and less pessimistic about the economic outlook – almost all respondents (96%) were gloomy about the UK economy six months ago, while 70% still are today. Economic pessimism in the Netherlands has also fallen, whilst business optimism in both countries has risen.

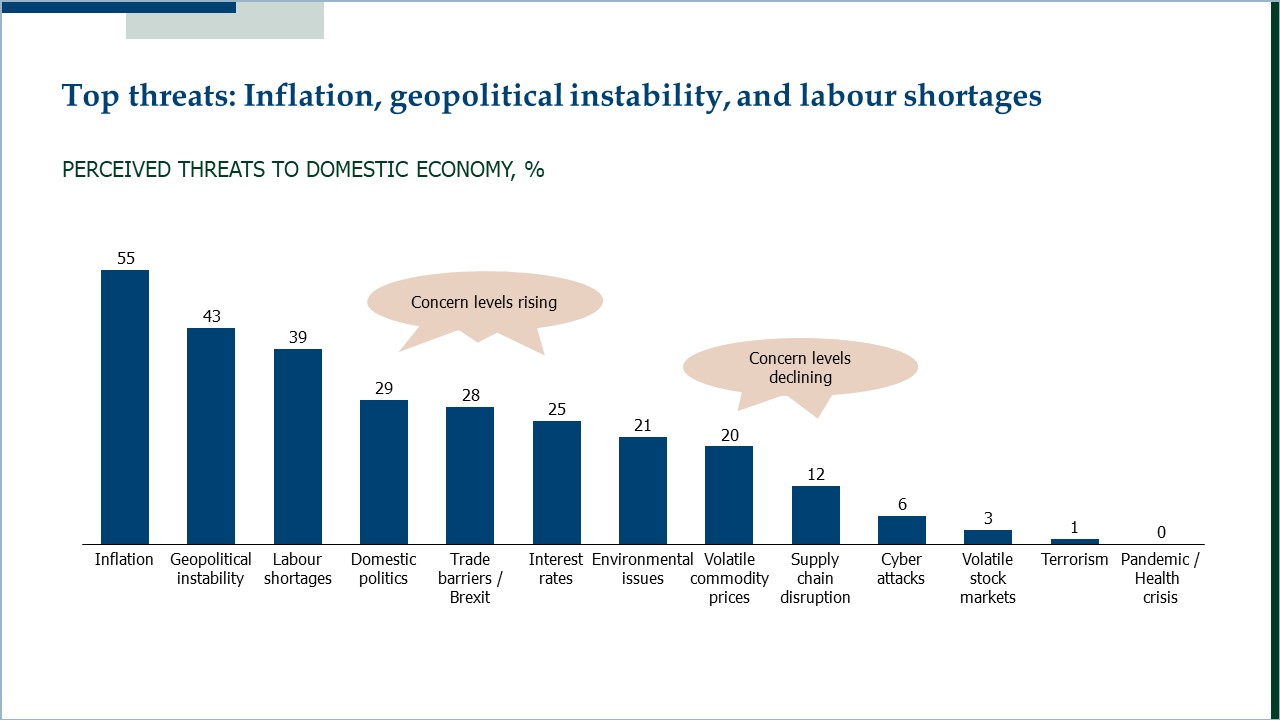

In terms of threats to the domestic economy, overall, inflation remains the top concern, followed by geopolitical instability and labour shortages, with concern around volatile commodity prices and supply chain disruption falling quite significantly (both are c. one-third lower than last quarter). UK business leaders continue to see trade barriers as a top threat, while environmental issues and domestic politics have become greater threats for Dutch business leaders.

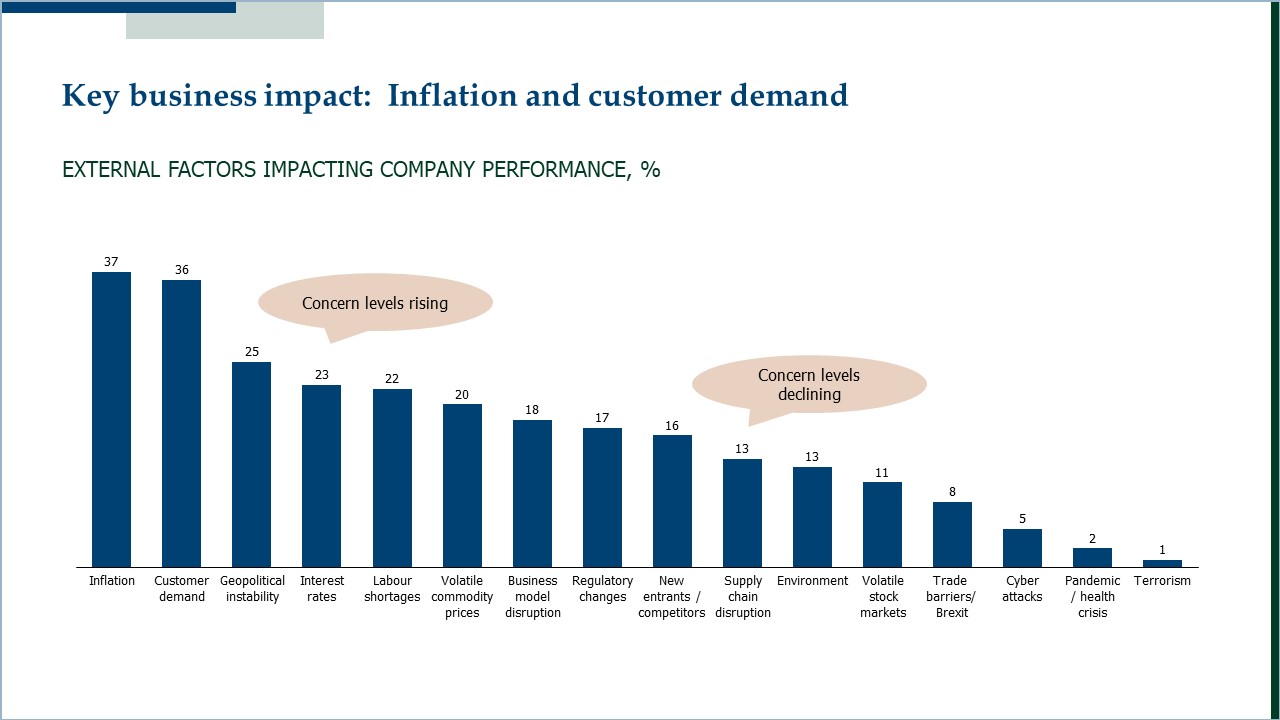

In terms of external issues facing their companies, inflation and customer demand remain the top issues, whilst labour shortages and supply chain disruption are now seen as less likely to have an impact on company performance. But there is also bad news in the mix: rising interest rates have become a more prominent factor and a greater cause for concern (23% citing this as an issue, up from 13% three months ago) – which is not surprising as rates in many economies continue to rise in the face of persistent inflation.

For all respondents, talent remains the most important internal issue. There has also been a marked increase in the importance of cost reduction, data optimisation/use of AI, and international expansion. By country, international expansion has increased in importance in the UK in particular. In the Netherlands cost reduction has risen up the agenda most notably.

Deep dives

In this survey we also took a closer look at three pressing issues: the cost of living crisis, new or changing ways of working, and the adoption of generative AI.

Cost of living/inflation

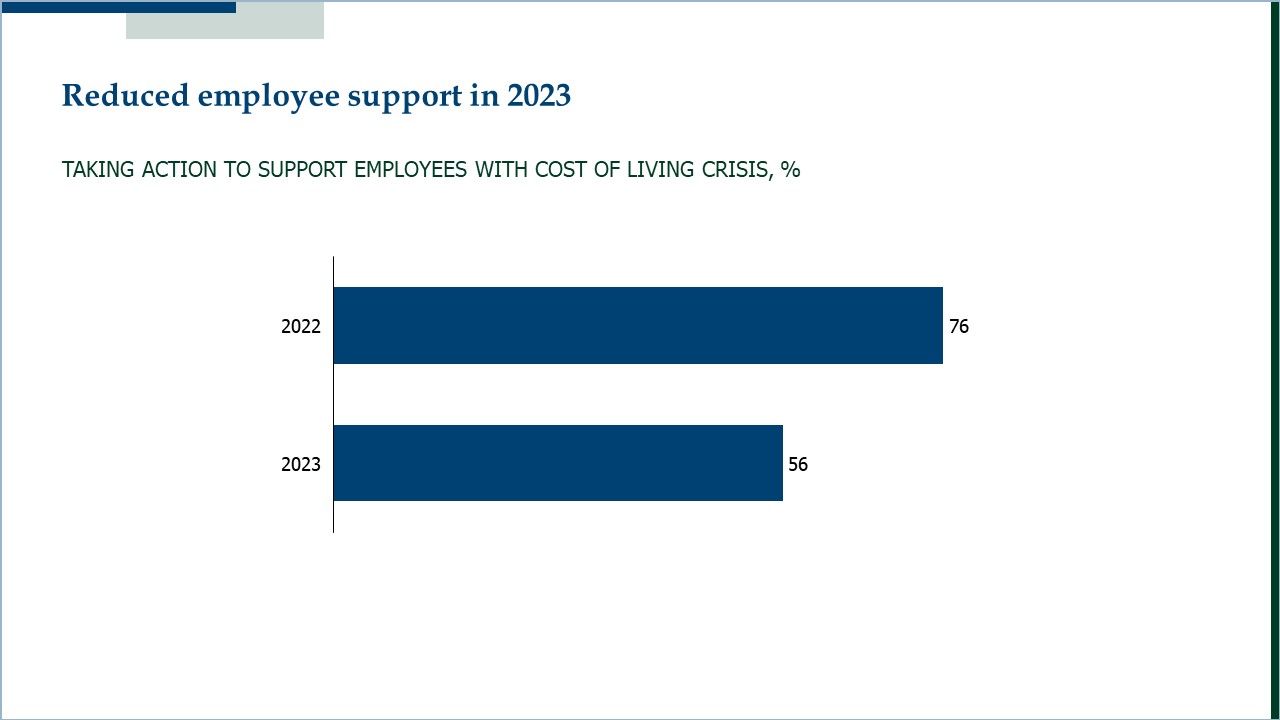

There is perhaps slightly more hard-headed realism – or at least less generosity – among business leaders at the end of Q2 2023. While three quarters of companies (76%) took some action in 2022 to help employees in response to the cost of living crisis, just over half (56%) have or intend to in 2023, despite the fact that inflation remains high. One in four companies are planning salary increases now compared with six in ten last year, and the number of companies making a one-off payment to help employees has fallen dramatically to 9% in 2023 vs 34% in 2022.

Ways of working

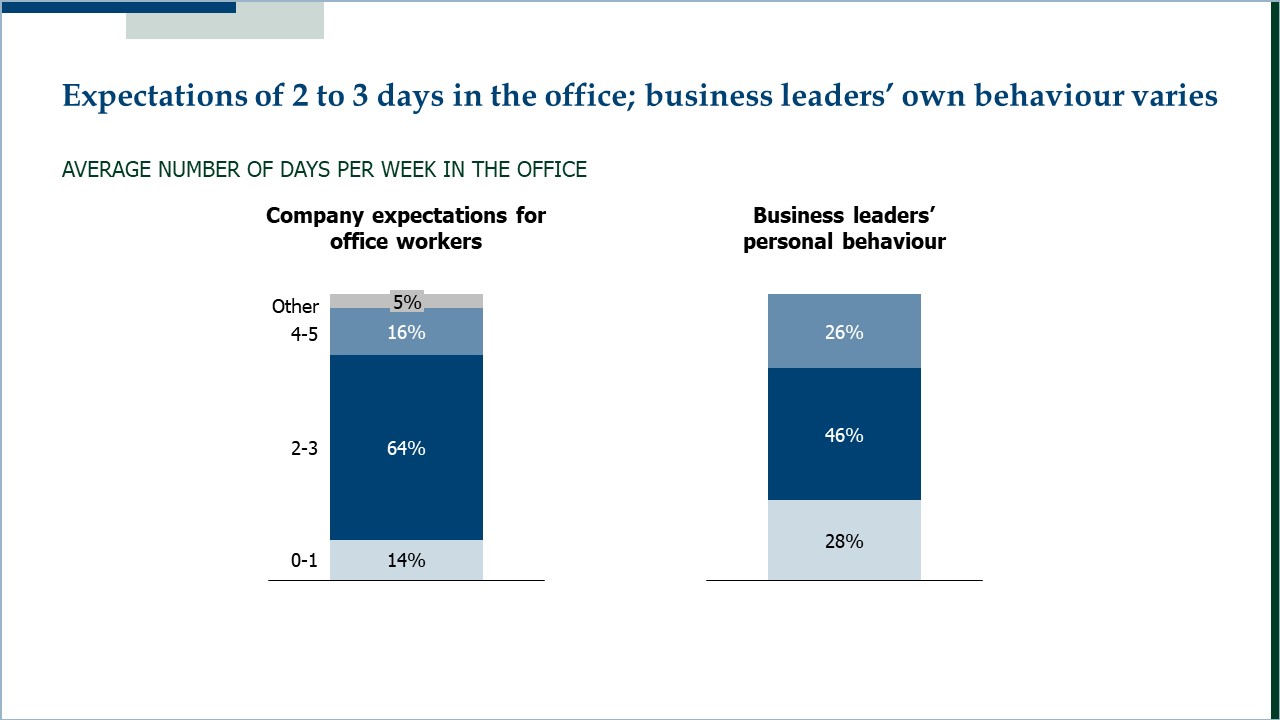

In terms of working patterns, there has been a small increase in full time office work since the end of 2022. However, nine in 10 companies continue to take a hybrid or flexible approach.

While most business leaders (62%) expect remote working to be largely unchanged over the next 1 to 3 years, three in ten expect their organisation’s approach to involve more office working over this period. But interestingly, while office workers are expected to be in the office 2 to 3 days per week, business leaders themselves exhibit more varied behaviour, with half also coming in 2 to 3 days per week and about a quarter barely in at all (1 day or less per week) and another quarter in the office almost full time.

Generative AI

Generative AI, such as ChatGPT, is clearly on the agenda for many. Nearly four in 10 companies currently consider generative AI important to their business or organisation, and projecting forward over the next 1 to 3 years six in ten consider it important.

Of the companies that are taking action about generative AI now, half are observing what others are doing, exploring, or experimenting with use cases. Those companies that currently view generative AI as important are more actively engaged in developing proprietary and open source tools, as well as recruitment and acquisitions.

* * *

Dena McCallum, co-founder of Eden McCallum, says that this latest set of data presents a somewhat mixed picture of current business sentiment. “It’s something of a conundrum,” she says. “While it is encouraging to see levels of pessimism fall, there is still clearly only limited confidence about the future, at least as far as the big picture is concerned. The most hopeful sign is that many leaders remain optimistic about the prospects for their own business over the next 1 to 2 years. We are hearing in the market an expectation that Q4 this year will see a turning point,” she adds.

To view the full results, please click here.

Follow us on LinkedIn to remain updated.