Consumer Sentiment Survey Q3 2023

Consumer sentiment has been on something of a rollercoaster ride over the past few years, as first Covid and then war in Europe shattered both economic expectations and purchasing power. The latest Eden McCallum survey of consumers in the UK and the Netherlands confirms that the mood is shifting again.

Around 1,500 UK and Dutch citizens were asked to share their views on global, domestic and personal prospects and to describe how their spending decisions have altered over the past three months. What emerges is a picture of careful consumers, displaying increased optimism compared with a year ago, but still wary about many of their spending choices.

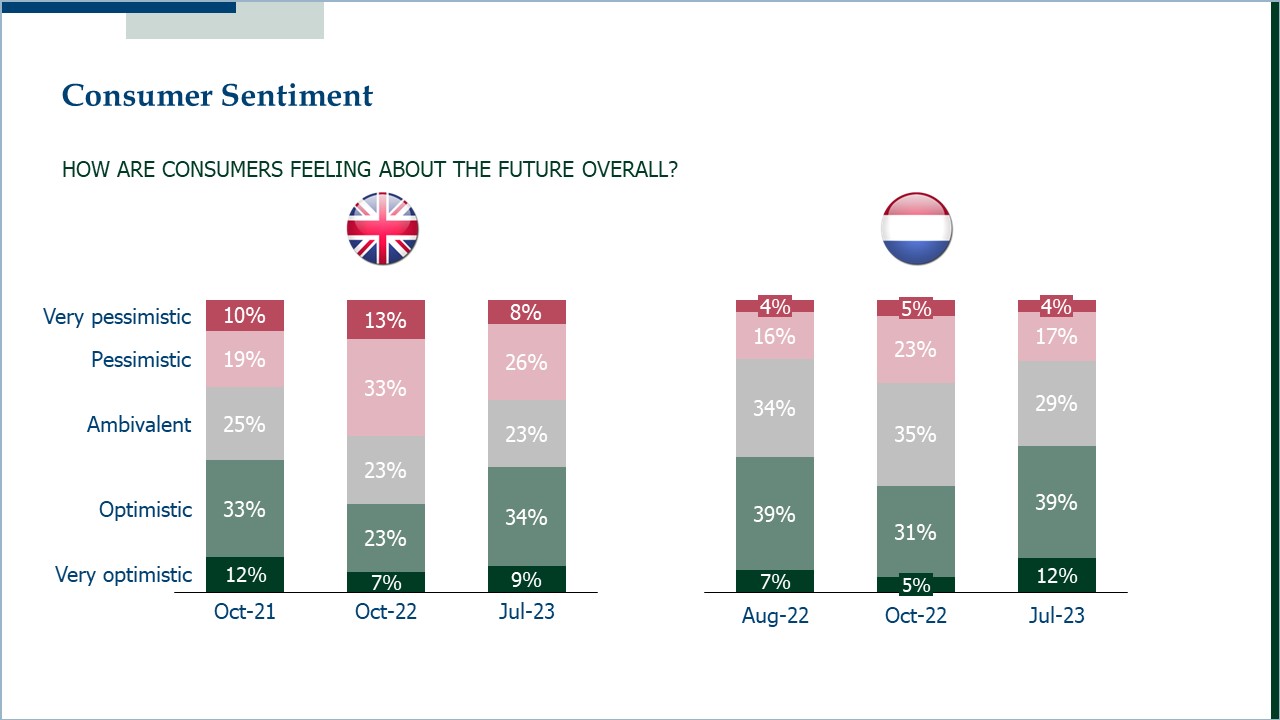

Throughout the survey, the mood is consistently gloomier in the UK than the Netherlands, unsurprising given the differing economic and inflationary contexts. In the UK c.35% of respondents are pessimistic about the future overall, higher than the c.30% who felt this way in 2021, but down from the c.50% recorded in October of last year. In the Netherlands pessimism is lower, and back to 2021 levels, at around 20%, down from a peak of c.30% in last October.

In the UK the chief cause for concern is the domestic economy. Three quarters of respondents (74%) said they were worried about it compared to half (49%) in the Netherlands, where global conflict was the biggest worry (at 64%).

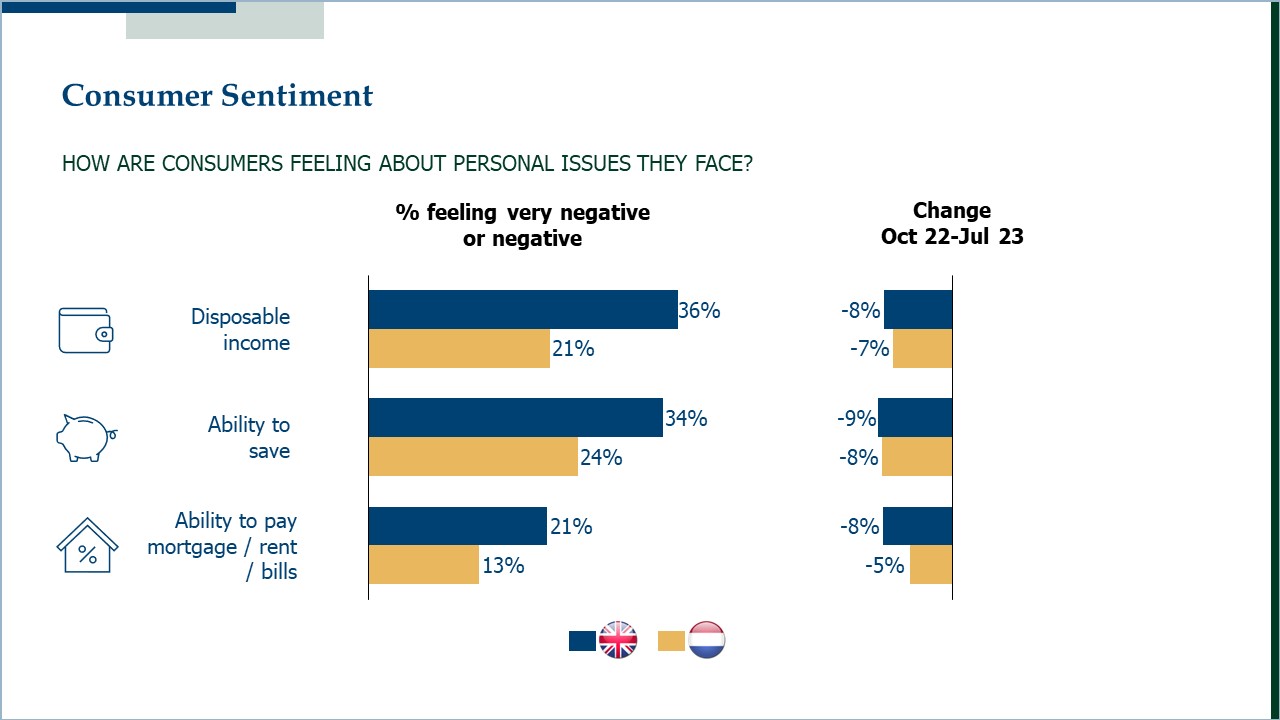

Despite concern about global and domestic issues being high, respondents in both markets are relatively more positive about most aspects of their personal lives, such as health, career prospects and job security. The ability to save and spend remains the main concern, with around a third of UK respondents and a quarter of Dutch worried, although these figures are about 10 ppt lower than those recorded in October 2022.

Although concerns have eased, worries about disposable income continue to translate into changing spending decisions, particularly in the UK.

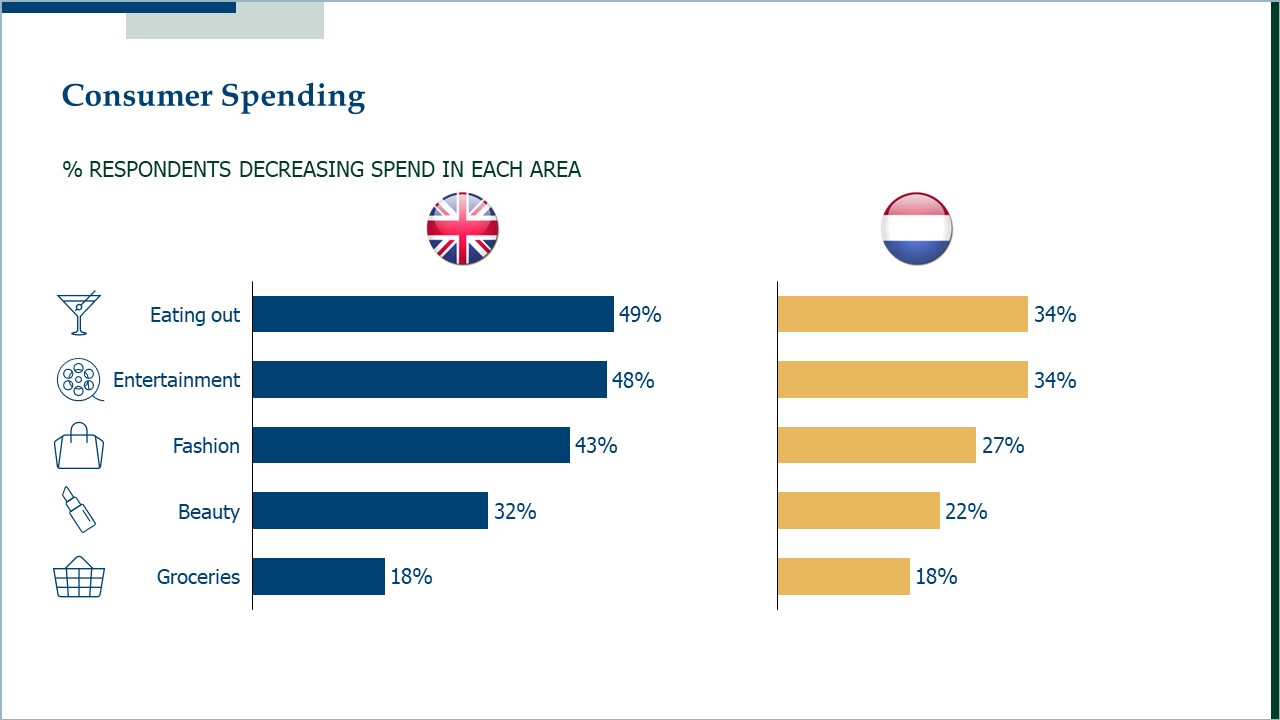

In the UK, at least a third of respondents say they have spent less over the past three months on all categories tested, apart from the ‘essentials’ like groceries, broadband and mobile. Takeaways, eating out and entertainment outside the home faired worst, with c.50% of respondents cutting back, followed by fashion, sports & leisure equipment, and alcohol & tobacco, where close to 40% of respondents said they are spending less. Buying fewer items and shopping less often was the main way consumers report they are spending less.

The picture in the Netherlands is less stark, with the proportion of respondents cutting back c.10-20 ppts behind the UK in most areas, although the pattern is similar, with non-essential categories being the key area for tightening belts.

Grocery is the #1 area in which respondents are spending more (c.40% in the Netherlands and c.50% in the UK), driven by price increases, which are also the main reason behind the increase in spend reported in other categories.

Sara Ghazi-Tabatabai, Partner at Eden McCallum, says the shifting mood of consumers presents a challenge to businesses. “While there are some welcome signs of an improvement in consumer sentiment, higher prices for food and other essentials are forcing consumers to hold back elsewhere. The market will remain challenging for discretionary items for some time. Having a competitive value proposition – and a streamlined operating model that delivers it – is more important than ever.”

To view the full results, please click here for the UK and click here for the Netherlands.

Follow us on LinkedIn to remain updated